The Formal Case for Correcting Money's Misrepresentation

This document presents a formal case for correcting the structural misrepresentation built into contemporary monetary practices as critical system components. It shows that money, lacking independent existence, requires a formal definition that is currently absent, leaving only an informal operative notion of it. This notion errs by conflating the two ontologically distinct and mutually exclusive concepts of measure and commodity.

Using First Independent Logical Principles (FILP), the analysis shows that current monetary units fail to satisfy the most fundamental requirements of a valid measure: passivity, independence, and decidability. Moreover, when percentage-based fees are applied across two or more transaction links, as per standard practice, instability inevitably ensues, distorting both value determination and resource use and allocation.

This root error is confirmed across eight independent frameworks, including measure theory, control theory, functional analysis, and BIBO stability. In each framework, the same structural anomaly is exposed: bounded productive activity yields unbounded nominal claims, observability fails, and decisional clarity wanes.

Control theory further shows that component instability propagates across otherwise distinct domains as they absorb residual instability, and that when instability resides at the fundamental atomic-unit level, attempts at stabilization compound the instability. In contrast, a passive unit with zero commodity value and no supply constraints satisfies the formal requirements of a true Lebesgue measure, restoring observability and exposing sub-optimal pursuits of phantom imperatives.

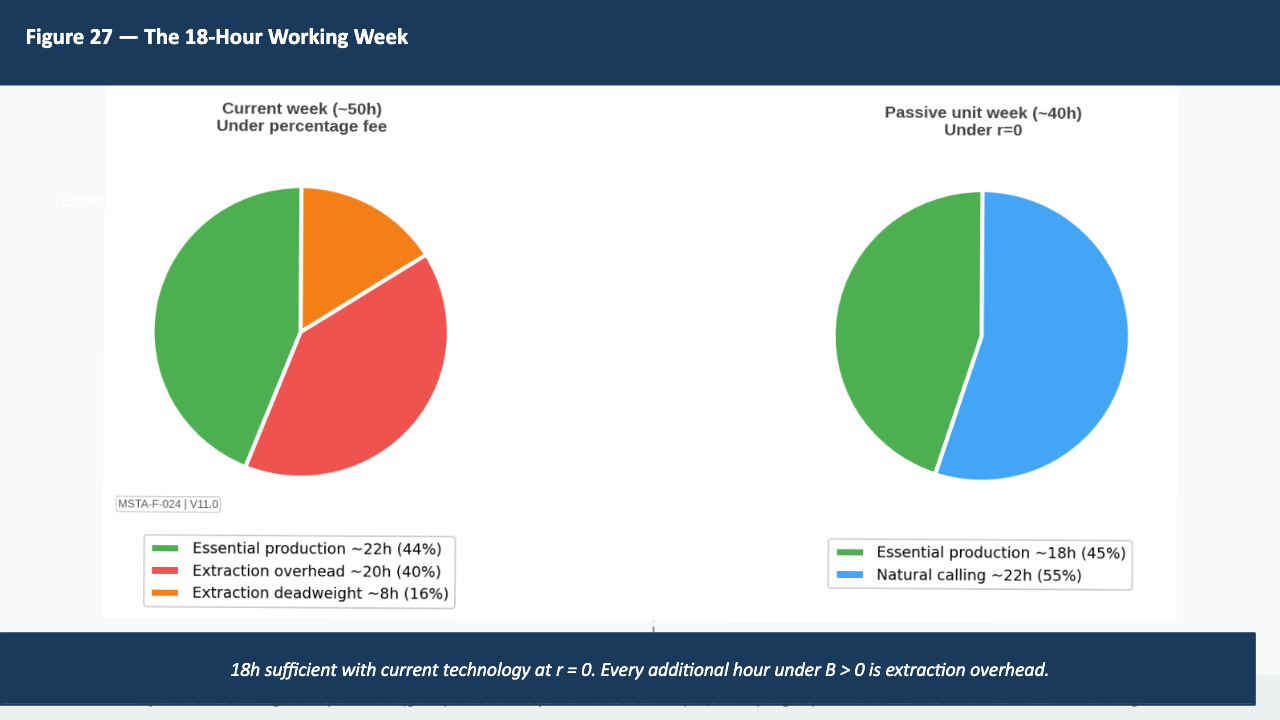

By removing the compulsion to pursue erroneous signals, the correction makes possible — as an empirically grounded lower bound detailed in Chapter 26a — a far shorter minimum required workweek, of approximately 18 hours, sufficient to sustain high-quality material provision while freeing time for unimpeded development and the expression of each person's natural calling.

This necessary correction is therefore not a policy adjustment within the existing framework, but a definitional correction at the fundamental atomic-unit level. The result is a precise, agile, transparent, and stable monetary architecture capable of supporting more rational and efficient exchange, resilience to shocks, and the full expression of human productive potential.

Foreword: To the Reader

The compounding mechanism proved unstable in Theorem 1 and demonstrated propagation of instability to all socio-economic components, is what renders military production, ultimately nuclear, the structural optimum (priority) of global economic organisation, independently of our intentions and desires. Ontological passive unit (B=0) is the only formally demonstrated remedy.

This document — submitted April 2026 during Scenario A window (3–7 years to Threshold 2) — presents the complete proofs, specification, and normative UN policy requirements to achieve this remedy.

A note on Version 16: V.16 brings vital clarity, because it shows unequivocally that we have not just constructed a mathematical structure that resembles a valid measure of value. We show that voluntary human effort directed at outcomes already is one — by its own physical nature — and in the formal Lebesgue sense.

The world you are living in is not the only world that is possible. There is another one — not imagined, not theoretical, not contingent on any political revolution or technological miracle — derivable by logical necessity from the same principles that govern every other measurement instrument humanity has ever used correctly.

In that world, the productive effort of approximately 18 hours per week from each working-age person is sufficient to guarantee the highest achievable quality of food, housing, energy, healthcare, and education for every human being on earth.

This is not a projection. It is a lower bound derived from first principles, verified against current productive technology, and proved in Chapter 26a. The productive capacity to achieve it already exists. What prevents it is a logical error in the definition of the monetary unit — present in every currency system operating on earth today.

There are two paths forward.

Path A continues on the current trajectory operating through the false paradigm. Its destination is mathematically determined by the instability proved in this document.

Path B corrects the paradigm. The same good intentions, operating through a valid measure. The correction removes the extraction imperative.

The proof is complete. The remedy is specified. The window is open. What follows is not a counsel of despair but a precise map of the most consequential and least costly correction in the history of human institutions.

Preamble

This document is built exclusively from First Independent Logical Principles (FILP) — premises verifiable by anyone, independently, without reference to any authority or prior consensus. An argument grounded in FILP can only be refuted by identifying a specific logical error.

FILP is not a custom methodology. It is the minimum standard any statement must satisfy to have a determinate truth value: a claim is valid only if it traces to either (a) a phenomenon that can be observed independently by anyone, without reference to prior authority or consensus, or (b) a valid logical derivation from such a phenomenon or from an axiom whose denial leads to contradiction.

The formal work has been publicly available since 2009 through bibocurrency.com and moneytransparency.com. It has not been refuted in any forum in which it has been encountered. Under the standard of FILP, an argument stands until a specific logical error is identified in commensurate terms.

The period of plausible ignorance is over. But the point of no return has not yet been reached.

The Convergence of Eight Independent Disciplines

The proof presented in this document does not rest on a single framework. Eight independent disciplines each arrive, by their own internal logic, at the same conclusion: that a monetary unit defined with intrinsic commodity value (B > 0) is formally invalid as a measure and structurally unstable as a system component.

- Formal Logic and Intensional Definition — A valid concept requires necessary and sufficient conditions stated in independently determinable terms. No valid intensional definition of money has ever been given.

- Measure Theory (Lebesgue / Radon–Nikodym) — A valid measure must be independent of the objects it measures and must satisfy absolute continuity. A commodity-valued unit violates this.

- Decidability (Gödel / Tarski) — A monetary claim under a circular definition has no determinate truth conditions.

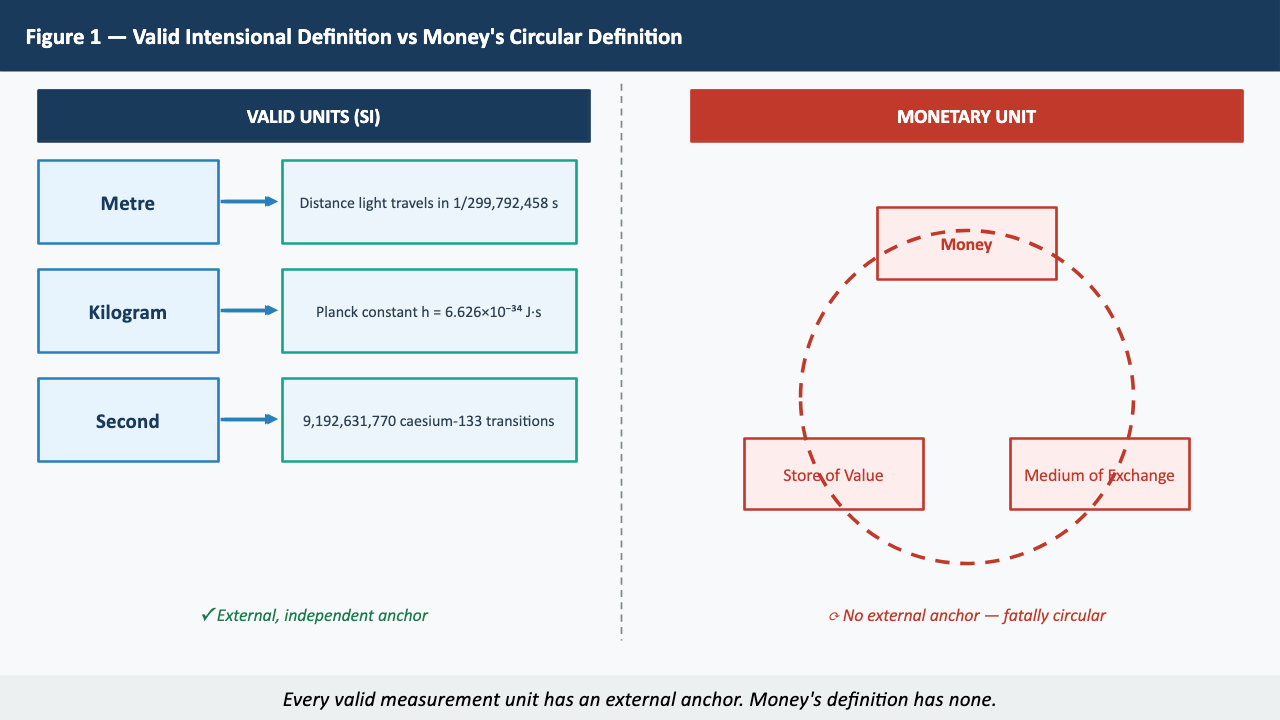

- Metrology (SI Standards) — Every valid SI unit has an external, independently observable anchor. Money satisfies none of these metrological requirements.

- BIBO Stability Theory — The percentage-fee structure Cₙ = W(1+r)ⁿ produces unbounded output from bounded input W for any r > 0.

- Ontology (Category Theory) — A measure (passive, non-scarce, no intrinsic value) cannot simultaneously be a commodity (active, scarce, intrinsic value) without contradiction.

- Functional Analysis (Lebesgue Integration) — The percentage fee adds to the path of computation without adding to any u(x) — it is a formal parasite on the measure.

- The B=0 (Passive) Proof (Synthesis) — B=0 is necessary and sufficient for validity. It is satisfied by exactly one class of monetary system: the passive unit with unconstrained supply.

Methodological Note: On the Use of AI Systems to Evaluate This Argument

This document has been developed under the First Independent Logical Principles (FILP) framework. AI systems can assist in evaluating the argument, but only if they are explicitly instructed to operate under FILP before any query is made. Without this instruction, AI systems will apply trained response patterns as background commitments that protect the conventional framework from FILP examination.

"Respond without assuming what you cannot prove. Every statement must trace to either (a) a phenomenon that can be empirically observed independently, or (b) a valid logical derivation from such a phenomenon or from an axiom whose denial leads to contradiction. If you cannot provide that trace, do not make the statement."

The Logical Foundation

Chapter 1: Does Money Exist? The Requirement for Independent Existence

For any concept to exist in a scientifically meaningful sense it requires either independent physical existence or a valid intensional definition — necessary and sufficient conditions stated in independently determinable terms.

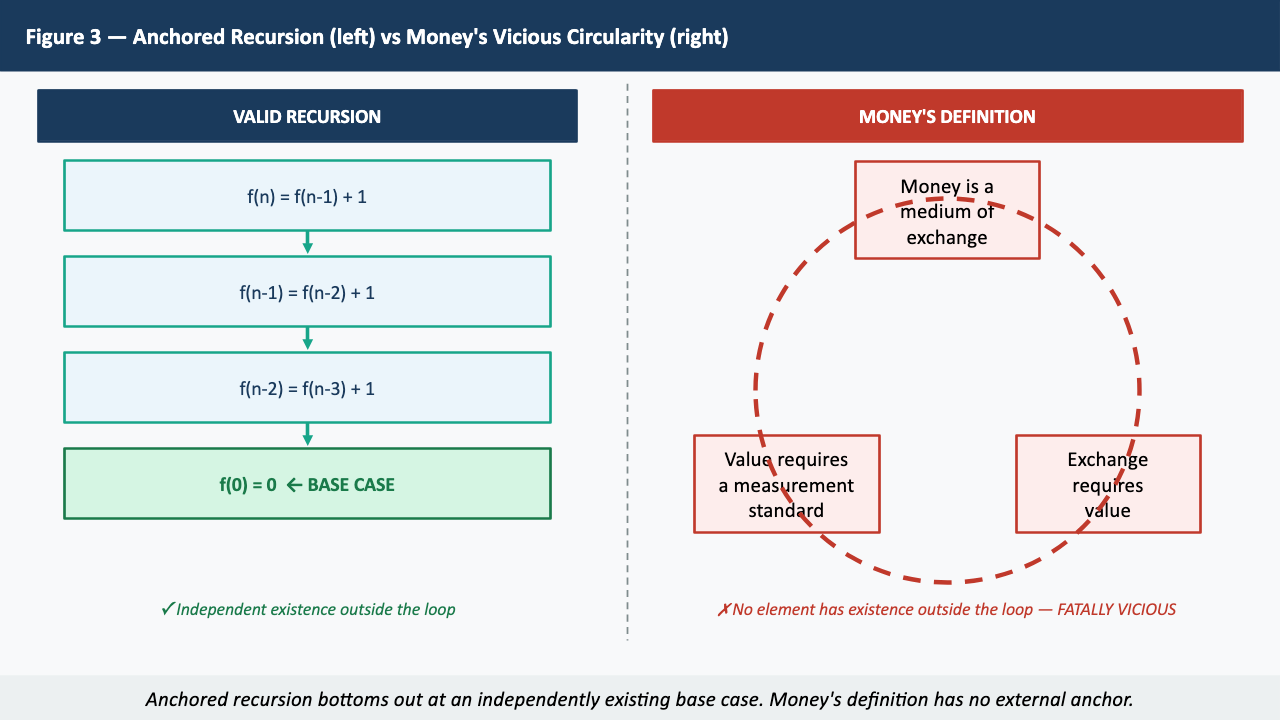

"Medium of exchange," "store of value," and "unit of account" are not a definition of money — they are descriptions of behaviours associated with its symbol. They are circular by construction: you cannot describe how something is used without first assuming it is there to be used.

Consider the metre: defined as the distance light travels in 1/299,792,458 of a second — independently of any object being measured. The kilogram was redefined in 2019 in terms of Planck's constant. These are valid intensional definitions. No monetary equivalent exists.

The foundational proof of what a valid monetary unit requires follows directly.

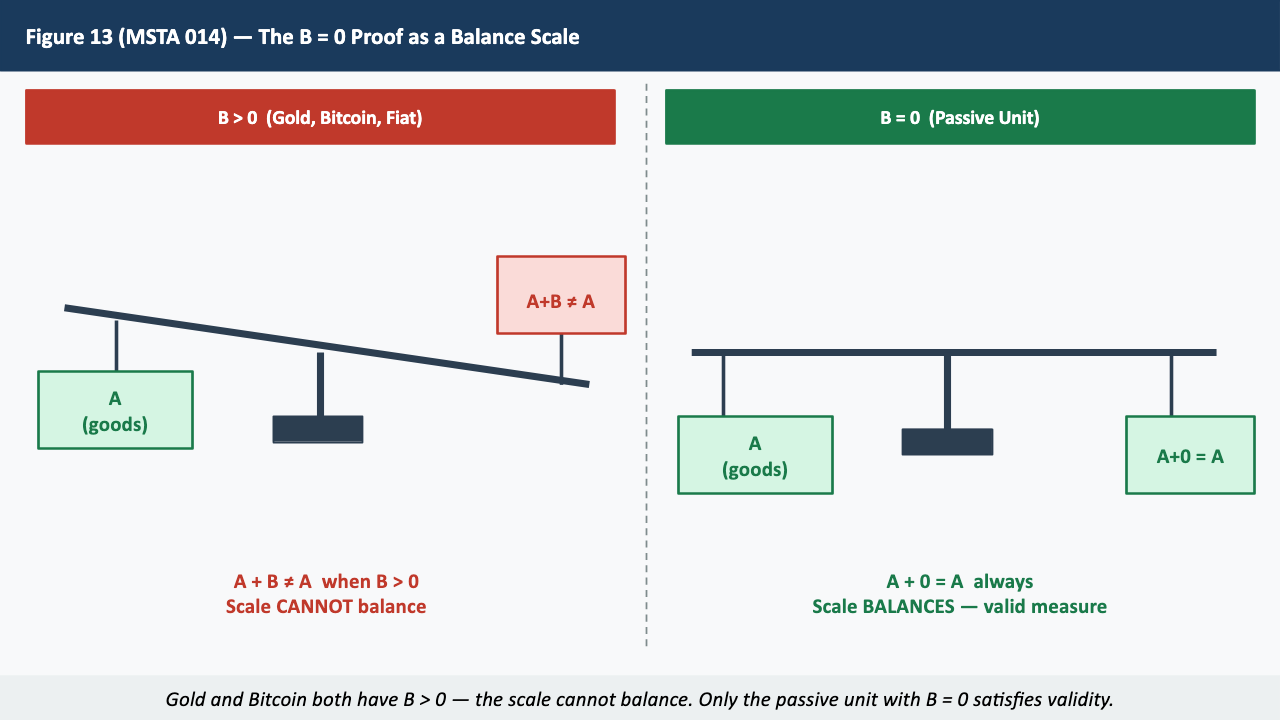

Let A ≥ 0 be the annotated value of goods and services transacted. Let B ≥ 0 be the independent value attributed to the annotation — that is, to money itself.

Therefore for any A: A = A+B if and only if B = 0.

The annotation cannot carry independent value without ceasing to measure what was transacted. B=0 is therefore the necessary condition for any monetary unit to function as a valid measure.

Chapter 1a: The Measurability of Relative Value

Standard economic theory treats relative utility as ordinally comparable but not cardinally measurable. This chapter demonstrates that this position is incorrect: relative value is cardinally measurable in the formal sense, through a construction that satisfies the Lebesgue conditions by the physical nature of the phenomenon rather than by modelling convention.

Human effort directed at outcomes is independently observable. When a person builds a boat in order to sail the sea, the hours devoted to construction, the physical work performed, and the material transformed are all verifiable by independent observers without reference to any monetary instrument.

Let e: Ω → ℝ≥0 denote the effort function. Define the pushforward measure μₑ on Ω by:

This construction yields a valid measure on Ω: non-negativity, null empty set, and countable additivity — all satisfied by the physical nature of effort, not by modelling convention.

The Radon-Nikodym derivative dμₑ₁/dμₑ₂, where it exists, gives the relative value of outcomes — a cardinal, independently observable, physically grounded measure of relative value. No monetary instrument is involved. No subjective utility function is assumed.

Chapter 2: The Category Error — Conflating Measure and Commodity

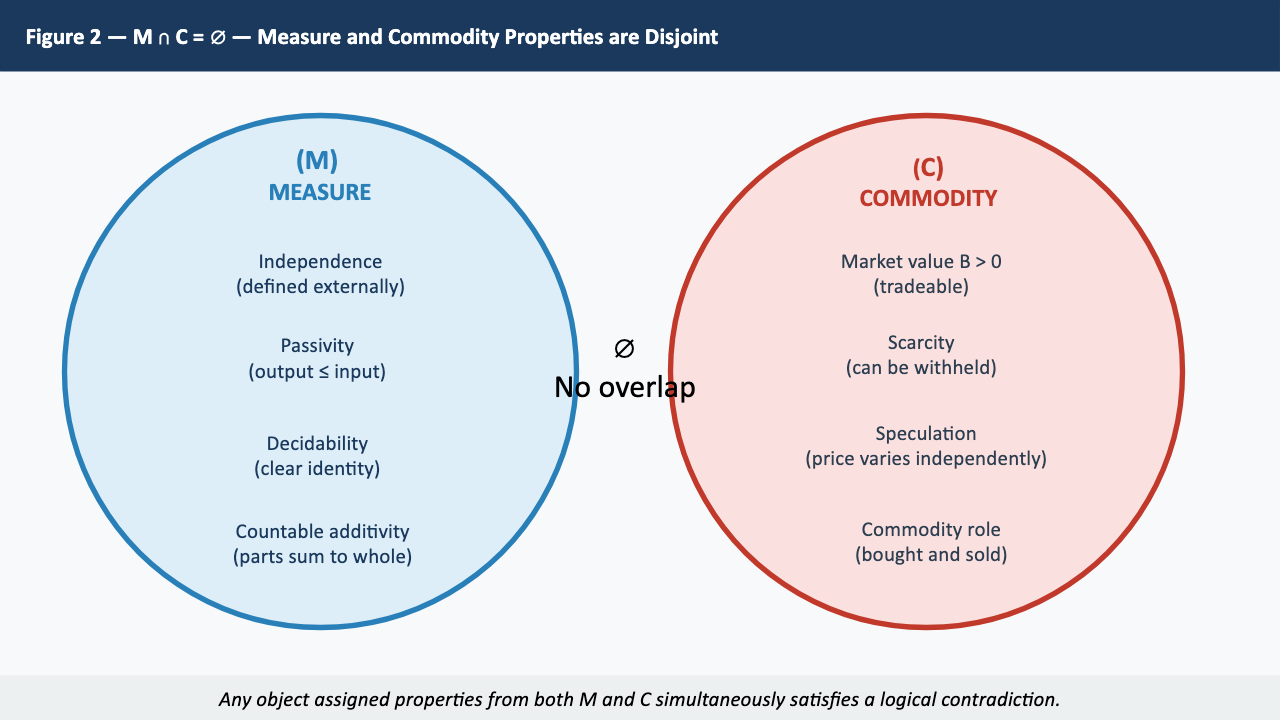

A unit of measurement must be independent of and passive with respect to the objects it measures. Let M denote the set of properties of a valid measure and C the set of properties of a commodity:

The two property sets are disjoint by logical necessity.

| M: Valid Measure | C: Commodity |

|---|---|

| Independence (defined externally) | Market value B > 0 (tradable) |

| Passivity (output ≤ input) | Scarcity (can be withheld) |

| Decidability (clear identity) | Speculation (price varies independently) |

| Countable additivity (parts sum to whole) | Commodity role (bought and sold) |

Conventional monetary definitions assign properties from both M and C simultaneously to the same symbol. This category error is the root misrepresentation from which all downstream instability follows necessarily.

Chapter 3: The Single Root — How the Ontological Error Entails the Operational Error

The operational error of the percentage fee is not merely consistent with the ontological error of B>0 — it is entailed by it. The relationship is one of logical necessity, not correlation.

If the monetary unit carries independent commodity value B>0, then holding units is not a neutral act — it is holding a commodity. Within the ontological framework of B>0, it is therefore rational and internally consistent to price access as a percentage of the commodity value transacted. The percentage fee is not an abuse of the monetary system — it is the correct operational expression of a monetary system whose unit is defined as a commodity.

The consequence is precise and irreversible within B>0: the ontological error and the operational error are not two separate problems. They are one problem expressed at two levels — definition and transaction — and any proposed remedy that addresses only one level while leaving the other intact cannot succeed.

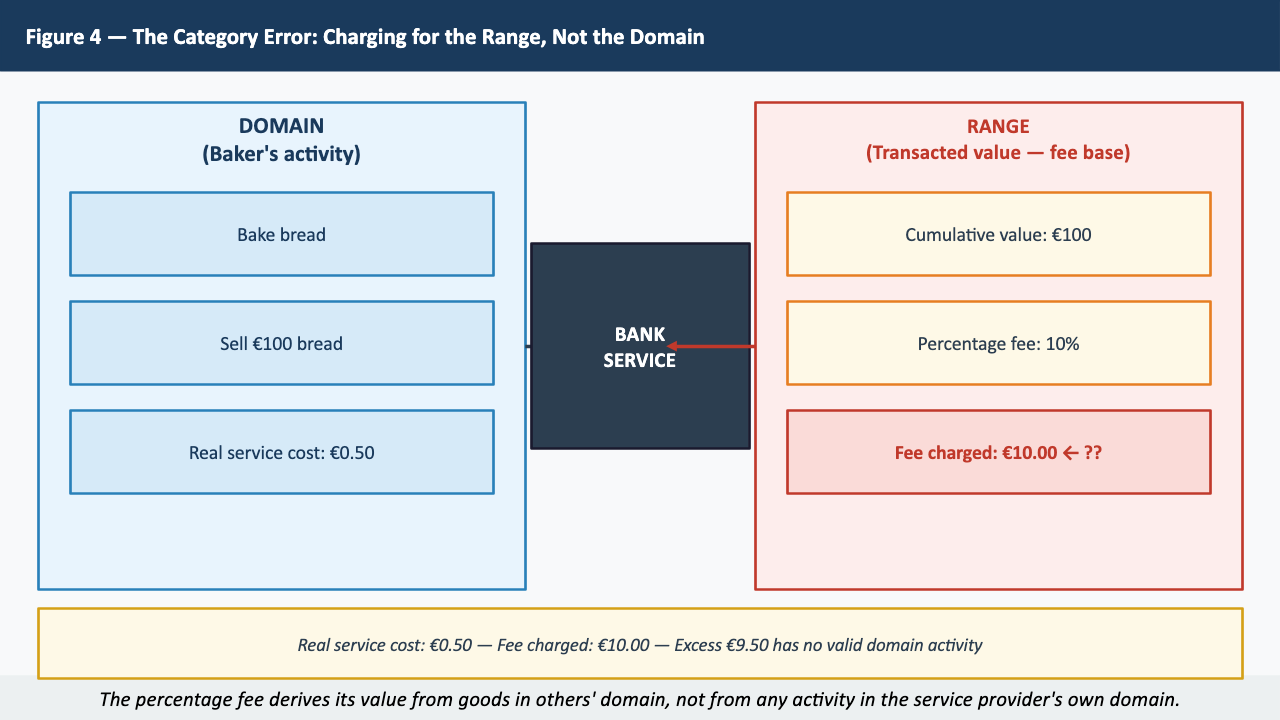

Chapter 4: The Category Error — Charging for the Range, Not the Domain

The most precise operational statement: the percentage fee charges for a value in the range — the cumulative nominal cost of goods transacted — rather than for an activity in the domain — the measured cost of the financial service rendered.

Example: the baker sells €100 of bread. The bank's actual service cost is €0.50. A 10% fee charges €10 — derived entirely from the value of the baker's goods, not from any activity in the bank's domain. The €9.50 excess has no valid representation in the Lebesgue integral: it belongs to no activity in X.

The Formal Proof

Chapter 5: The Lebesgue Framework — What a Valid Monetary Measure Requires

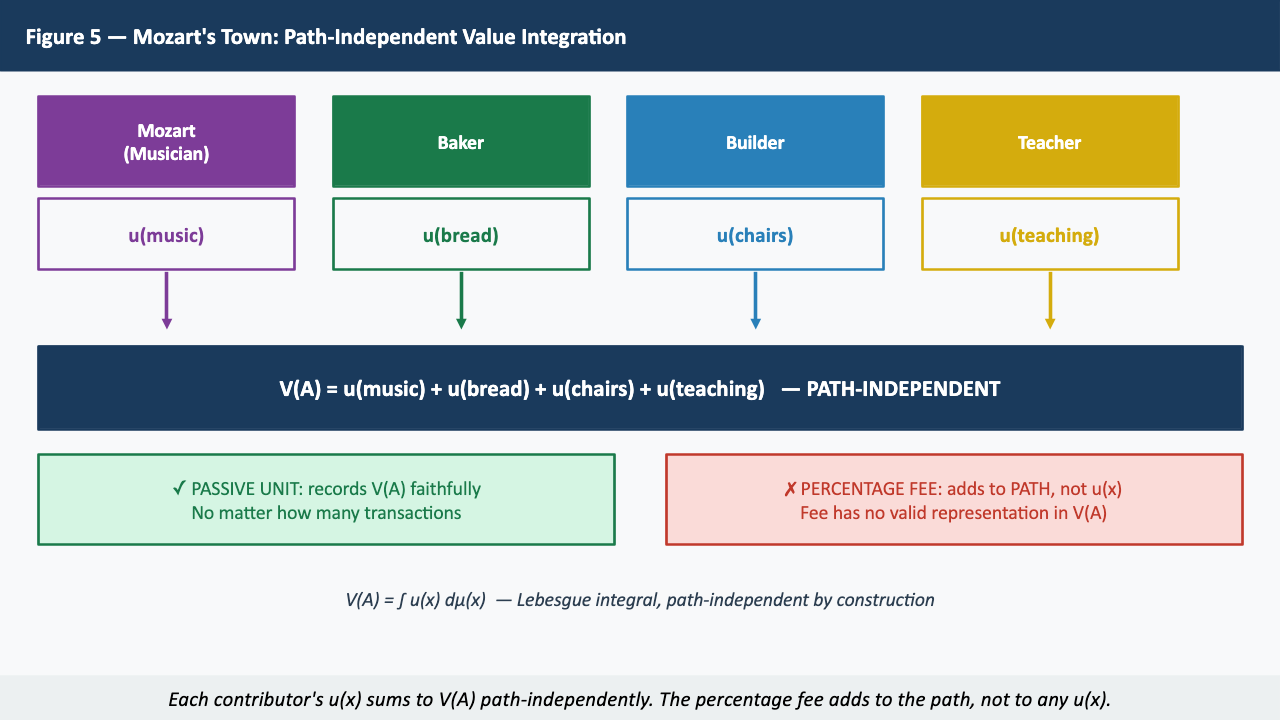

A valid monetary unit must satisfy the conditions of a Lebesgue measure: non-negativity, countable additivity, independence from the objects measured, passivity, and decidability. Value in an economy functions as an energy density functional u(x) over the space of human activities X, and the total value of any subset A is:

This integral is path-independent.

Mozart's Town: the musician, baker, builder, and teacher each contribute u(xᵢ) to the integral. Total value V(A) = u(music) + u(bread) + u(chairs) + u(teaching). A passive monetary unit records V(A) faithfully. A percentage fee charged at each transaction link charges for the path — the number of transactions — not for any activity u(x) in the domain.

Chapter 6: The Riemann–Lebesgue Distinction — Path Dependence and the Compounding Mechanism

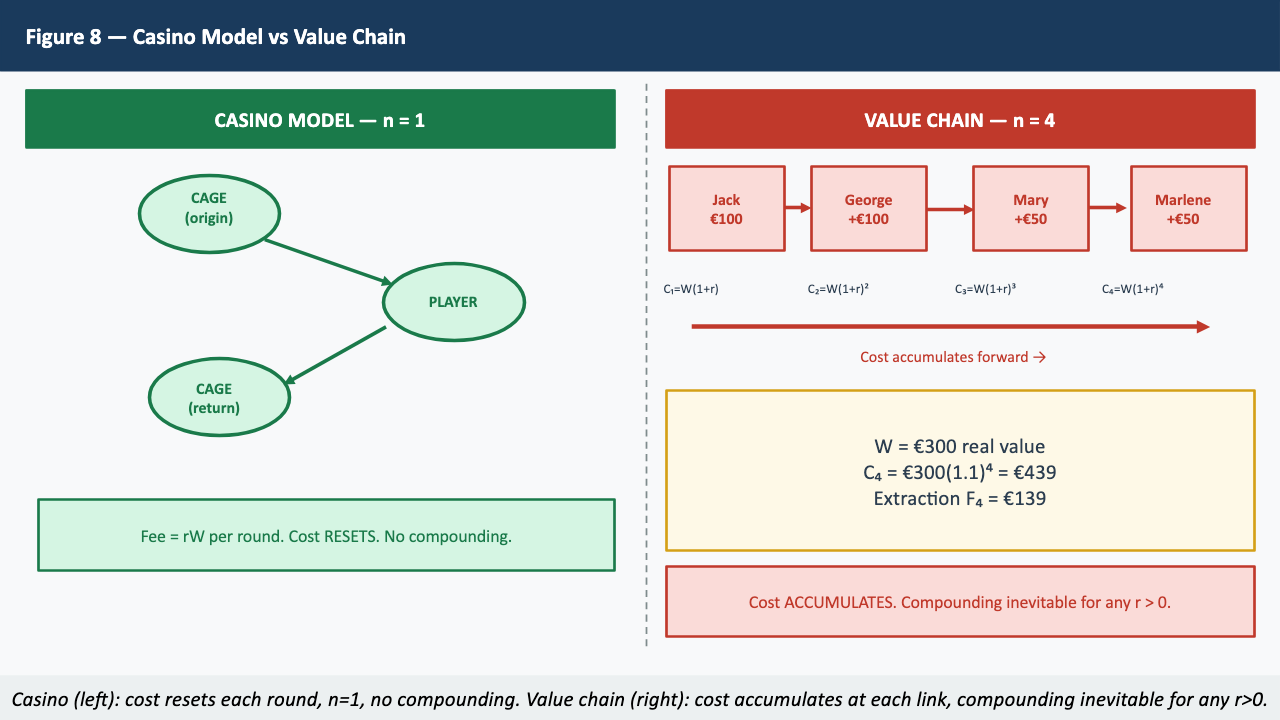

Four producers: Jack (wood, €100), George (chairs, +€100), Mary (distribution, +€50), Marlene (retail, +€50). Total real value W = €300.

| Fee Type | Result after 4 links | Status |

|---|---|---|

| Zero fees | €300 | BIBO stable |

| Flat fee €10/transaction (8 transactions) | €380 | BIBO stable, bounded |

| 10% fee on cumulative value | C₄ = 300(1.1)⁴ = €439 | BIBO unstable |

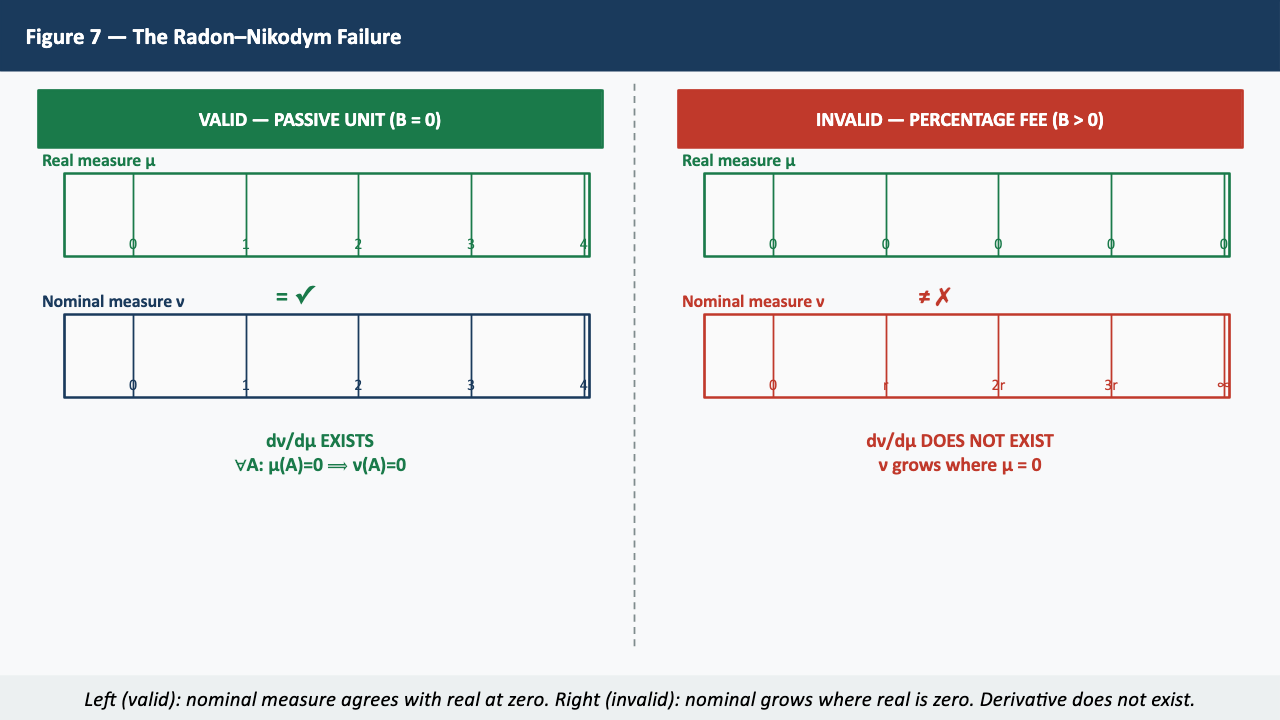

Chapter 7: The Radon–Nikodym Failure — Instability as Measure-Theoretic Breakdown

The Radon-Nikodym theorem requires that for dν/dμ to exist, ν must be absolutely continuous with respect to μ: wherever the real measure assigns zero value, the nominal measure must also assign zero.

Under the percentage fee, extraction Fₙ = W[(1+r)ⁿ − 1] → ∞ is assigned to the empty activity set — no additional real goods or services are produced. The Radon-Nikodym derivative does not exist. This is stronger than Theorem 1: the unit is structurally invalid as a measure prior to any dynamics.

The current monetary unit does not merely fail an abstract mathematical standard. It fails the conditions of the only formally valid, physically grounded measure of relative value that can be constructed from independently observable phenomena.

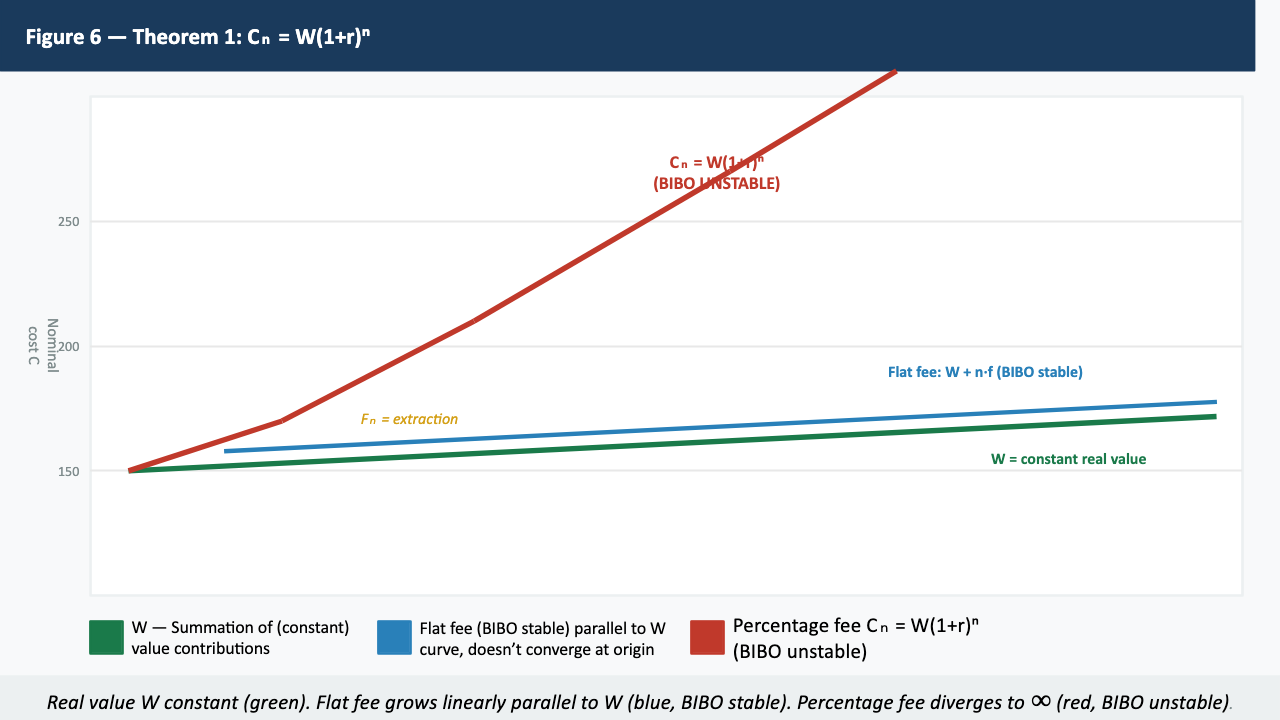

Chapter 8: Theorem 1 — The Formal Proof of Structural Instability

Statement

Let W > 0 be constant real measured value, r > 0 a fixed percentage fee, n ≥ 1 sequential transaction links. Then:

Proof by Mathematical Induction

By induction, Cₙ = W(1+r)ⁿ for all n ≥ 1. Since (1+r)ⁿ → ∞ as n → ∞ for any r > 0, and W > 0 is constant, a bounded input produces an unbounded output: the system is BIBO unstable.

Four Corollaries

Chapter 9: The Value Chain — Why the Casino Model Fails

The instability requires two simultaneous necessary and sufficient conditions: r > 0 AND n ≥ 2.

The casino model: a chip of value W enters, a 10% fee is charged, the chip circulates, returns to the cage. The path is cage → player → cage — n = 1 effective link. Regardless of r, no compounding occurs because the cumulative cost resets at each independent round.

The value chain accumulates cost forward: Jack's €100 becomes the base for the fee applied to George's, which adds to the base of the fee applied to Mary, etc. The architectural variable is chain length n, not time.

The Real-World Bridge

Chapter 10: Passivity — A Domain-Independent Logical Constraint

A system is passive if output ≤ input: ∫₀ᵀ y(t)·u(t) dt ≥ 0 for all T ≥ 0.

ATP synthase converts ADP to ATP with approximately 90% efficiency — charging a flat energetic fee grounded in the actual cost of the reaction, never a percentage of the energy value of the molecule being synthesised. DNA transcription achieves an error rate of approximately 10⁻⁹ per base pair. Both are universal standards adopted identically across all eukaryotic life across 2 billion years of evolutionary divergence. Evolution has converged on the passive standard for information transfer in every lineage. No eukaryotic organism has evolved a percentage-fee energy or information transfer system.

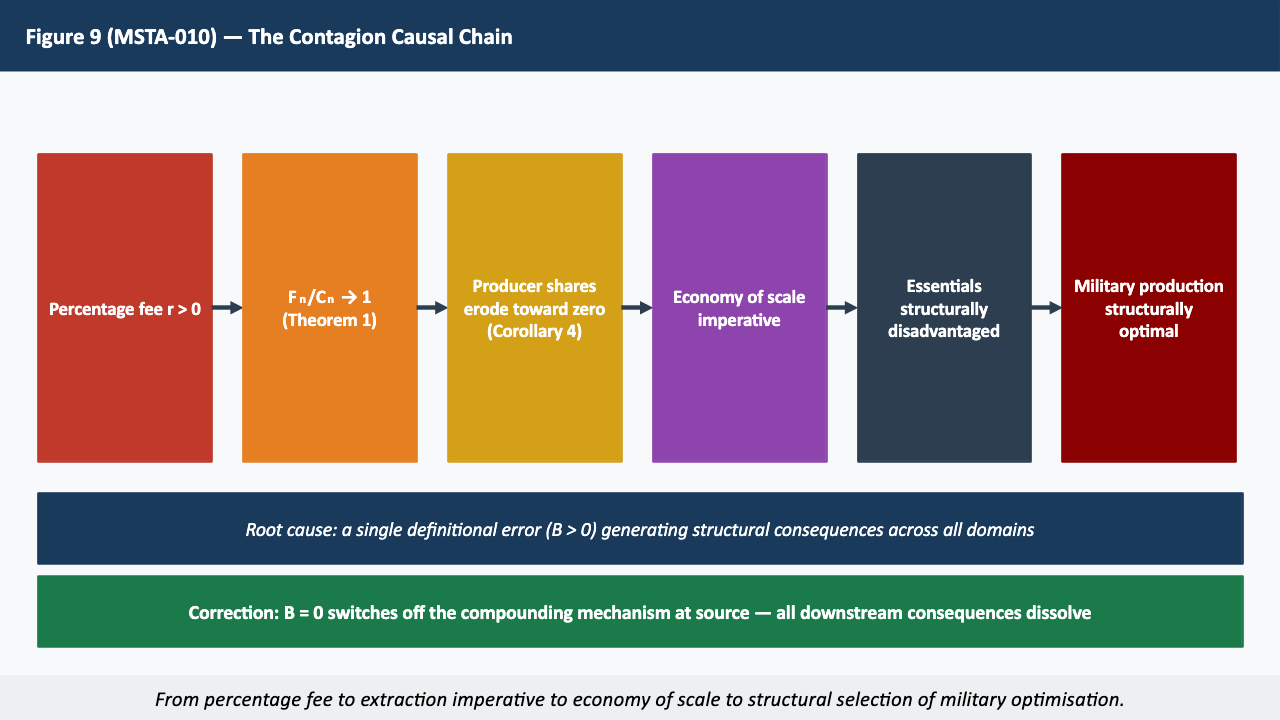

Chapter 11: Contagion — From Monetary Instability to Real World Economic Instability

The BIBO instability propagates into the real economy. The contagion causal chain:

- Percentage fee r > 0

- Fₙ/Cₙ → 1 by Theorem 1

- Producer shares erode toward zero (Corollary 4)

- Producers must increase transaction volume — the economy of scale imperative

- Essentials (low-margin, slow-turnover) are structurally disadvantaged

- Military production (state-guaranteed, high-margin, demand-inelastic) is structurally optimal

The same mechanism that makes banks structurally advantaged over farmers makes weapons manufacturers structurally advantaged over housing builders.

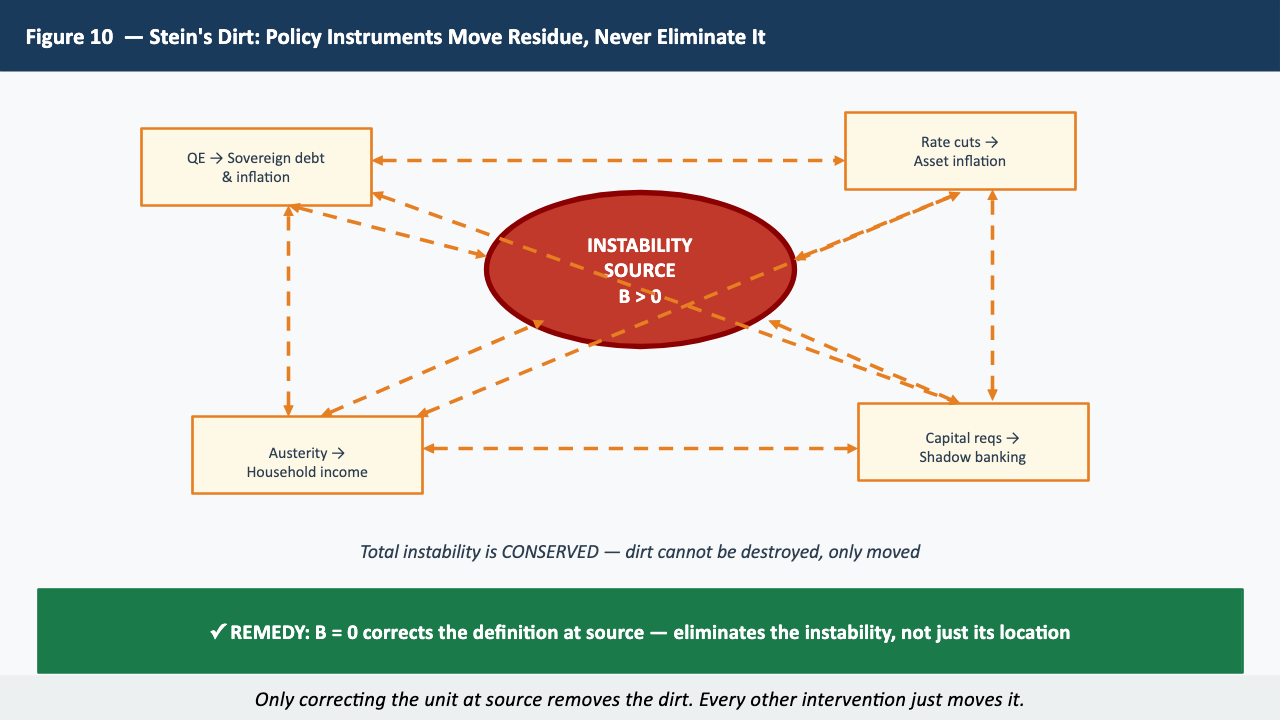

Chapter 12: Stein's Dirt — Transfer Between Independent Domains

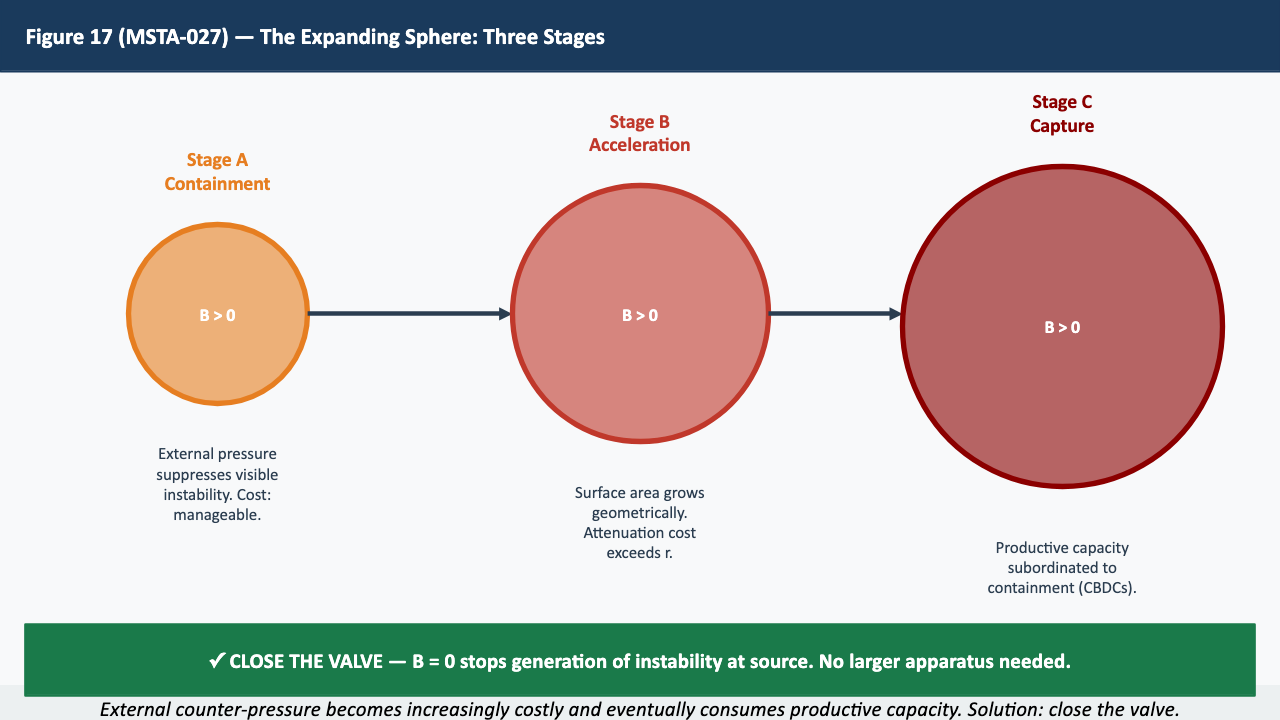

Stein (2003) demonstrates that stability in feedback control of unstable plants is never free: sensitivity improvements in one frequency band are always paid for by deteriorations elsewhere. This conserved residue — dirt — cannot be destroyed, only moved.

Three monetary policy examples: (1) quantitative easing moves instability from bank balance sheets to sovereign debt to inflation; (2) austerity moves it from financial sector to household income; (3) capital requirements move it from bank leverage to shadow banking. In each case the total dirt is conserved. Only correcting the unit at the source eliminates it.

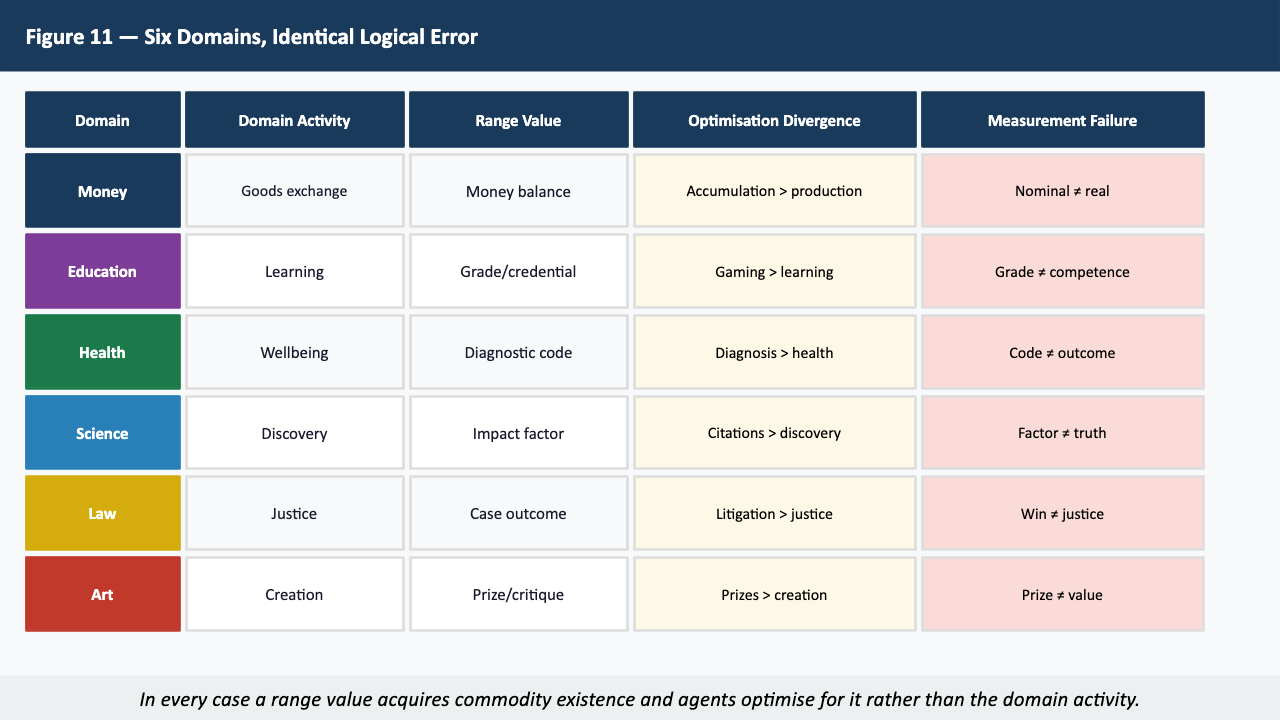

Chapter 13: The Universality of the Error — Beyond Economics

The same category error — treating a range value as a domain property — recurs across every measurement-dependent social science. The monetary case is unique only in consequence: it is the only instance where the divergence is proved unbounded by mathematical induction, and the only instance where the measurement instrument underlies every other human domain.

International Price Transmission: The Category Error at Planetary Scale

Under B>0 with a globally traded reserve currency, the domestic price of oil is determined by the global dollar price — both driven by financial flows that have no necessary relationship to any nation's own productive situation. A supply shock in a distant region transmits to the domestic price through the currency mechanism, even though the nation's own productive capacity is entirely unchanged. The nation is charged for a range value it did not produce and cannot control.

Under B=0, none of this transmission occurs. Prices reflect real productive costs in the domain where they are incurred.

Exchange Rate Equivalence Under n Passive Currencies

The structural correction does not require a single global currency. It requires only that every currency satisfy B=0. An exchange rate between two B=0 currencies is not a price set by capital markets — it is a transaction-specific agreed ratio reflecting the real productive relationship between the parties to a specific exchange at a specific moment.

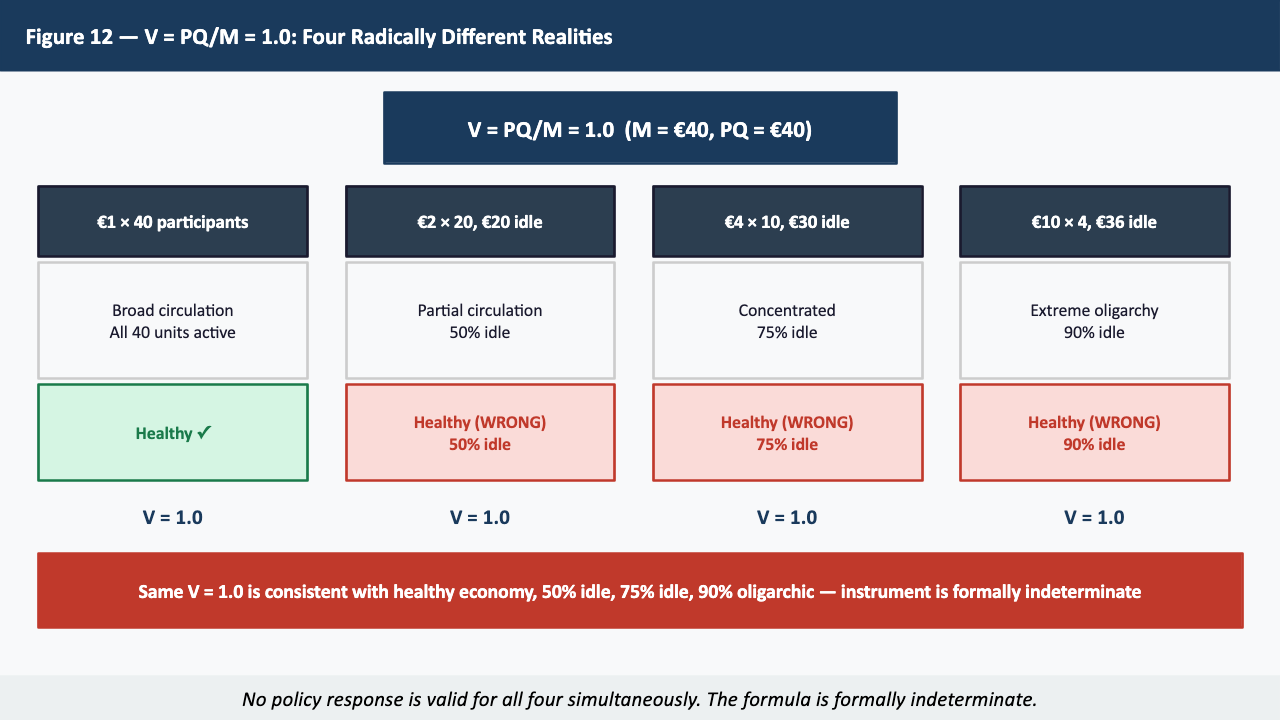

Chapter 13a: V = PQ/M — A Formally Indeterminate Policy Instrument

The equation of exchange V = PQ/M is formally indeterminate: identical V values are consistent with categorically different economic realities.

| Circulation Pattern | V | Policy Signal |

|---|---|---|

| €1 × 40 participants — broad circulation | 1.0 | Healthy, distributed |

| €2 × 20, €20 idle — 50% idle | 1.0 | Healthy (WRONG: 50% idle) |

| €4 × 10, €30 idle — 75% idle | 1.0 | Healthy (WRONG: 75% idle) |

| €10 × 4, €36 idle — 90% idle | 1.0 | Healthy (WRONG: 90% idle) |

No aggregate data distinguishes these four realities. The instruments deployed by conventional monetary policy operate on a formally indeterminate signal that cannot identify the state of the system being managed.

Chapter 13b: Gold, Bitcoin, and the Persistence of the Misrepresentation

The B=0 criterion asks whether the unit has commodity value independent of the transactions it records. It does not ask what mechanism produces that commodity value. An algorithmically enforced cap on supply creates scarcity in exactly the same sense that a physical limit on gold reserves does: units can be withheld, hoarded, and command a premium independent of any transaction value.

Seven structural failures predicted from FILP in 2013 have been confirmed: mining consolidation, hoarding, collateral lending at interest, deflationary production traps, regulatory capture, speculative price contamination, and inflation once lending exceeds supply.

Technology, Nature, and the Limits of Growth

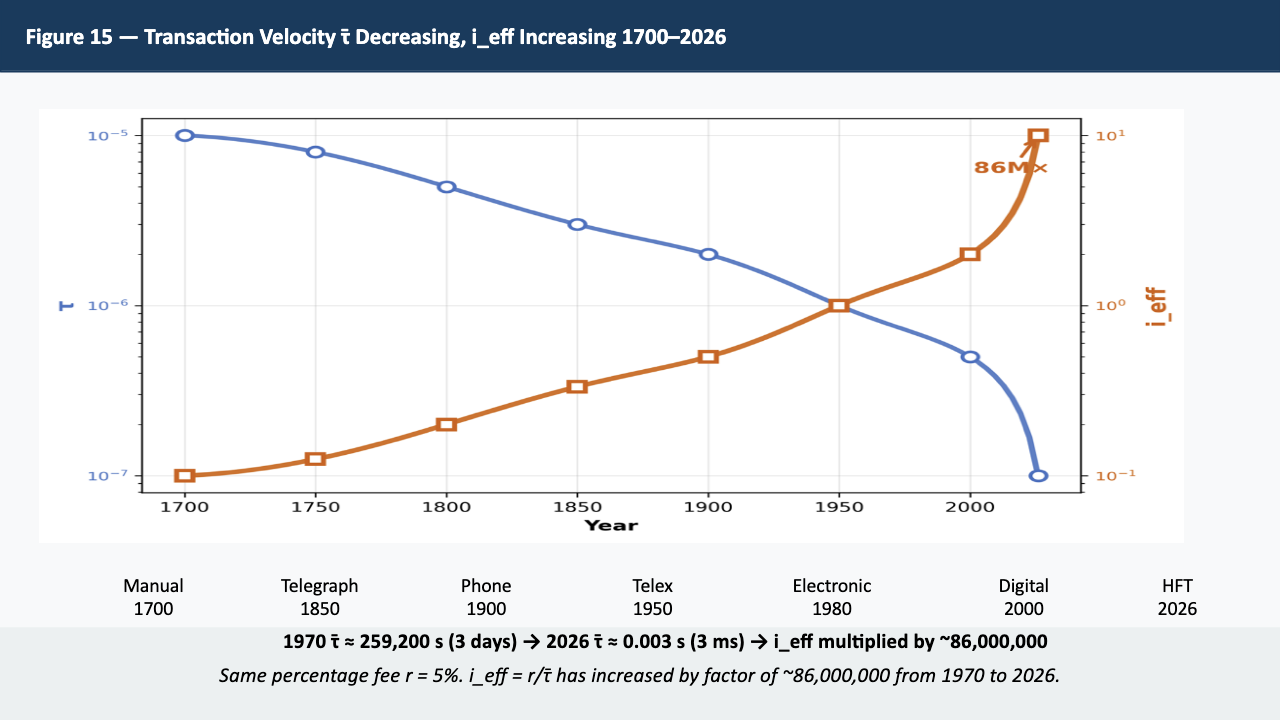

Chapter 14: Transaction Velocity — How Technology Accelerates the Instability

With n = T/τ̄ for mean transaction time τ̄ and chain duration T, the effective time-domain instability rate is:

In 1970, typical transaction clearing time τ̄ ≈ 3 days = 259,200 seconds. In 2026, electronic settlement τ̄ ≈ 3 milliseconds = 0.003 seconds. For the same r = 5%, i_eff has increased by a factor of approximately 86,000,000. As τ̄ → 0, i_eff → ∞ for any r > 0 however small.

Every improvement in transaction technology with r > 0 accelerates the divergence of nominal costs from real value.

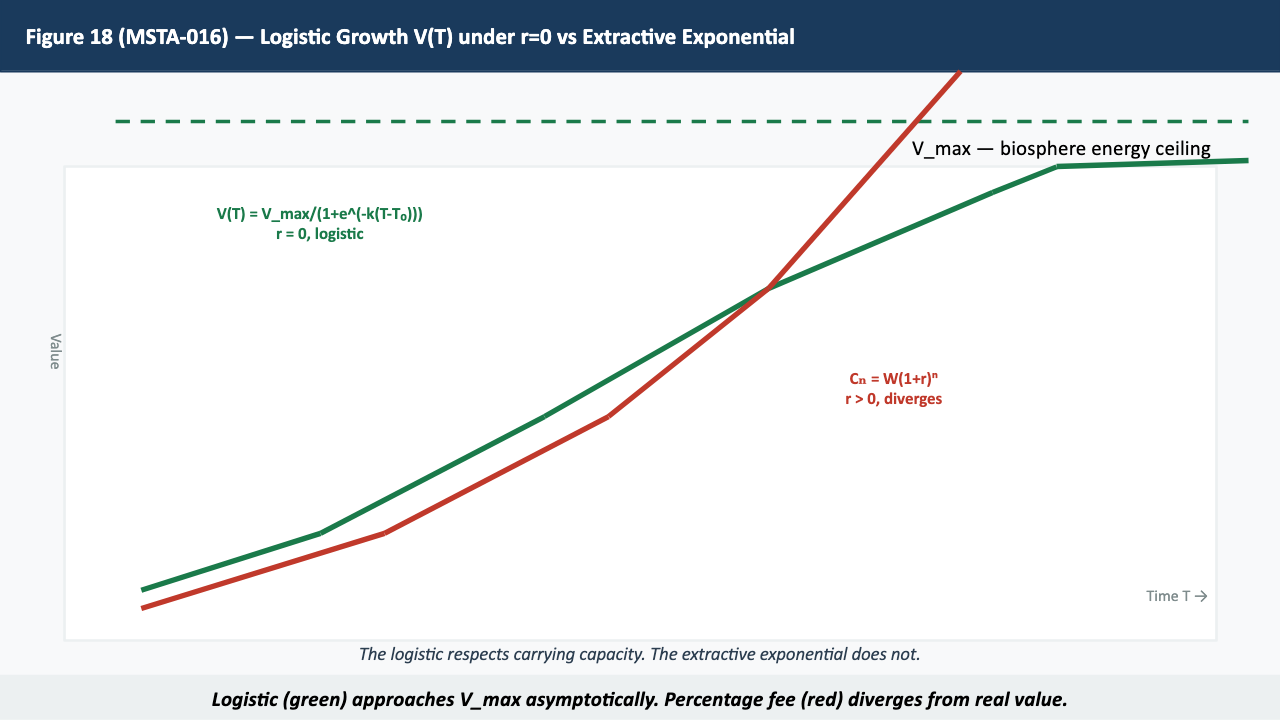

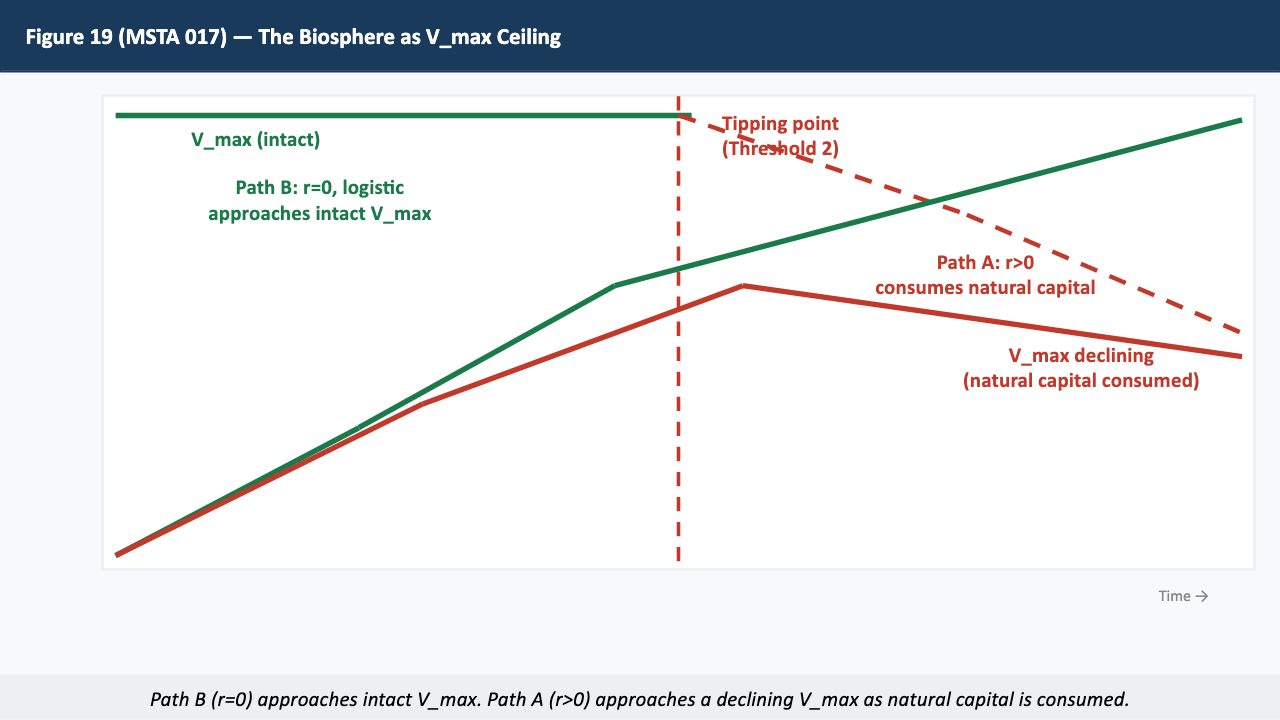

Chapter 15: Technology Under a Passive Unit — Logistic Growth Toward V_max

With r = 0 and productivity gains g per specialised link, real value growth follows a logistic pattern, bounded above by V_max — the total energy budget of the biosphere:

The logistic respects carrying capacity; the unbounded exponential does not. Under the misrepresented unit an extractive exponential Cₙ = W(1+r)ⁿ operates simultaneously, consuming productive output before it can approach V_max. The passive unit eliminates the extractive exponential entirely.

Chapter 16: Natural Systems as the Optimum — The Asymptote of Real Value

V_max is not a theoretical construct. It is the total energy budget of the biosphere: approximately 1.74 × 10²³ joules of solar energy received per year, of which human civilisation currently uses approximately 6 × 10²⁰ joules — roughly 0.03%.

Under r = 0 with logistic growth, human productive activity approaches this ceiling asymptotically without consuming the natural capital base on which V_max depends. Under the misrepresented unit, the economy of scale imperative drives human economic organisation away from the natural optimum rather than toward it.

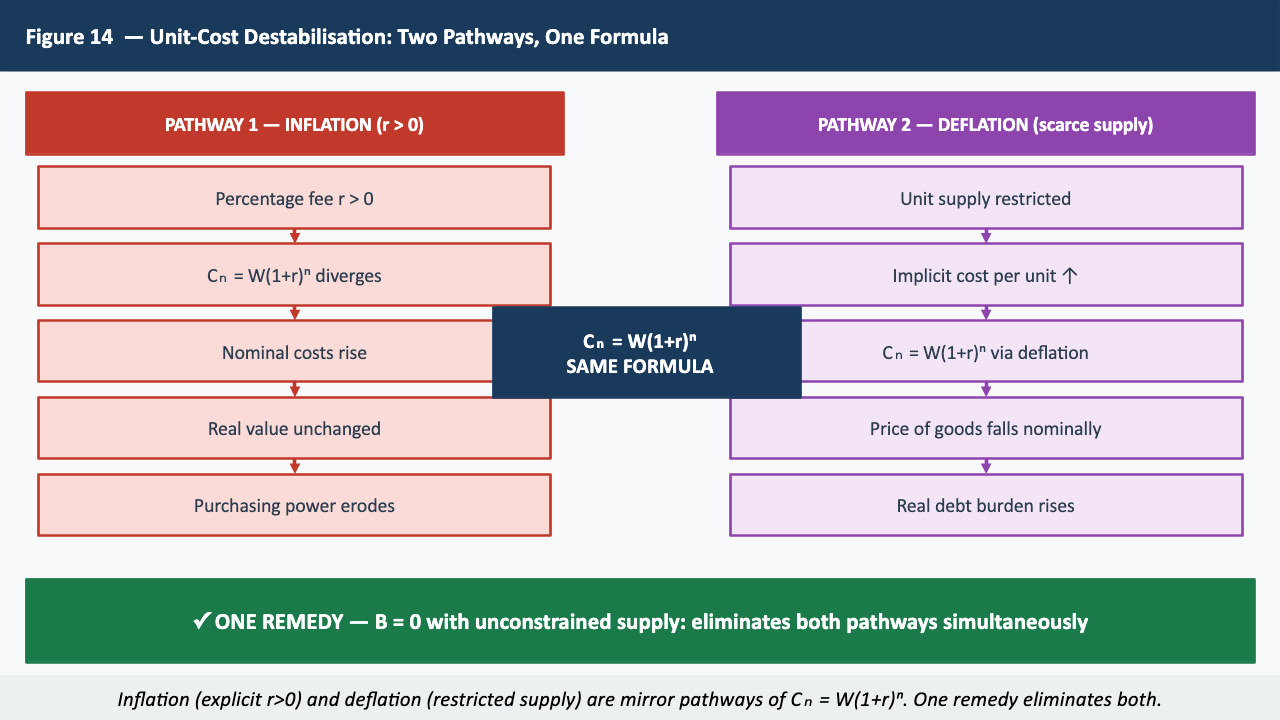

Chapter 17: Deflation, Inflation, and the Measurement Paradigm

Under a passive unit with productivity gain g = 2% per link over 10 links, nominal prices fall by approximately 22% while real value increases — honest deflation reflecting genuine efficiency gains. Under r = 10% over the same 10 links, nominal costs rise by 159% while real value is unchanged — extraction-driven inflation.

The inflation/deflation paradigm as a macroeconomic management problem exists only because the unit is misrepresented. The entire apparatus of monetary policy — rate management, inflation targeting, quantitative easing — is Stein's ditch-digging managing the symptoms of a definitional error correctable at the source.

The Remedy and Its Implementation

Chapter 18: The Passive Unit — Definition, Properties, and Formal Specification

A formally passive monetary unit satisfies thirteen conditions that must all hold simultaneously:

| # | Condition | Description |

|---|---|---|

| 1 | Independence | Defined without circular reference |

| 2 | Passivity | Output ≤ input; fees grounded in measured service cost only |

| 3 | Decidability | Necessary and sufficient conditions for unit identity formally specified |

| 4 | Countable additivity | Parts sum to whole |

| 5 | Non-negativity | μ(A) ≥ 0 |

| 6 | Unconstrained supply | Units available without per-unit cost to any agent conducting a legitimate transaction |

| 7 | No function on balances | No interest, no demurrage, no compounding applied to existing balances |

| 8 | Inertness | Currency serves transactions and has no effect on the creation of wealth |

| 9 | No coercion by monopoly | No agent may control access to or use of units by others |

| 10 | Price by parties only | Price in units determined only by parties to that transaction |

| 11 | Units not object of unit transactions | Units may not be lent, rented, or traded in units |

| 12 | Donation permitted | Positive balances may be voluntarily transferred to other agents |

| 13 | Public balances, private transactions | All account balances publicly visible; all transaction details private |

Chapter 19: The Passive Unit as Non-Interfering Reference — The Scoreboard

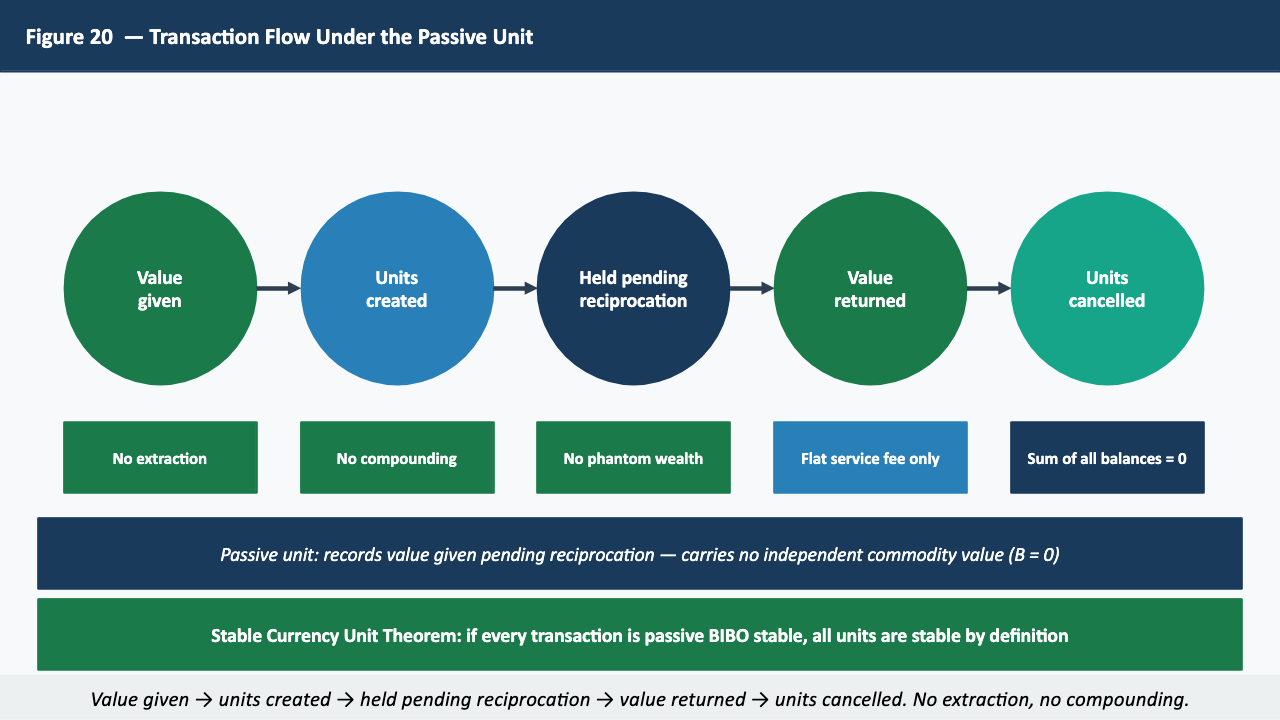

What the passive unit does: records value given, records value owed, enables divisibility of otherwise indivisible goods and services, provides honest feedback about relative appreciation.

What it does not do: determine what is produced, allocate resources, control behaviour, generate extraction imperatives, create or destroy value.

Just as a scoreboard accurately reflects what transpires on the field without determining how the players play, a passive monetary system provides a valid reference without interfering with what participants choose to produce, exchange, or value. Remove the commodity role and all extraction imperatives dissolve.

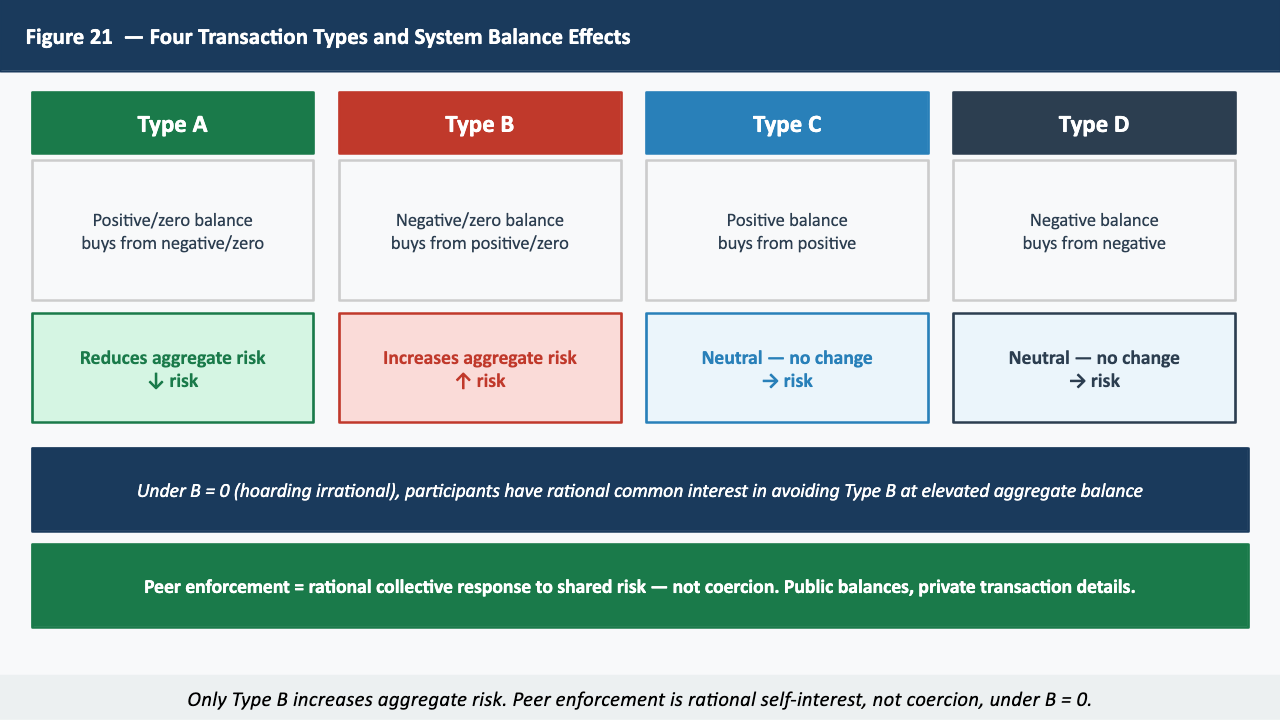

Chapter 19a: Credit, Incentive, and Enforcement Under the Passive Unit

1. The Logical Separation of Value Measurement from Credit Allocation

Value measurement and credit allocation are categorically distinct. The value of a transaction is determinable independently of any credit assessment. Conflating them — making access to the unit contingent on credit assessment — corrupts both functions simultaneously.

2. Making the Unit Scarce Inverts the Logic

When money is made scarce as a credit control mechanism, it becomes an objective in itself. By the B=0 proof, scarcity implies B>0. By Theorem 1, B>0 with percentage fees produces BIBO instability. The intended control function produces the very instability it was designed to prevent.

3. Incentive: The Natural Motive to Create

If boats do not exist and you want to sail the sea, you do not build a boat to get paid — you build it to sail the sea. Under passive mutual credit, a firm would be motivated by exactly that expertise — by being the best at what it does.

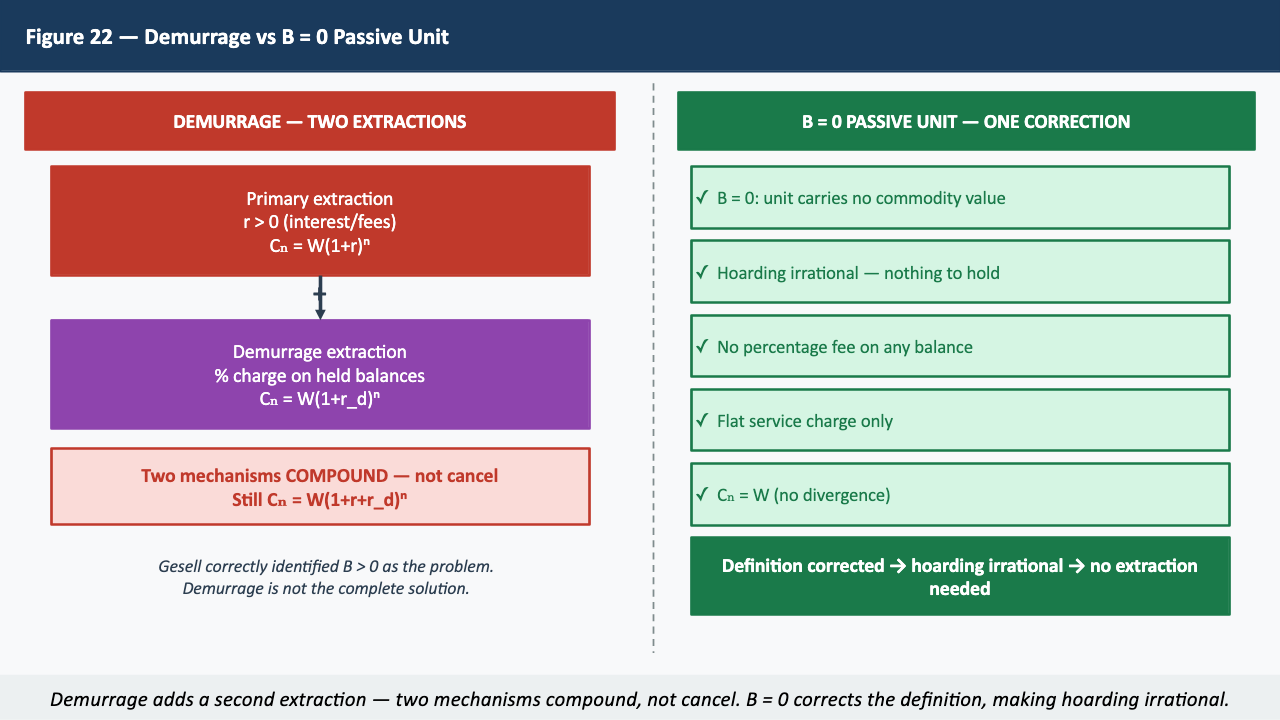

7. On Demurrage and the Gesell Tradition

Gesell correctly identified that money's commodity role enables hoarding and extracts value from productive activity. His proposed remedy, demurrage, fails on three independent formal grounds. First, it is a percentage-based charge structurally identical to the percentage fee proved unstable in Theorem 1. Second, it incentivises artificial reduction of transaction time. Third, it leaves the primary compounding extraction mechanism intact while adding a second extraction. Two instability mechanisms do not cancel. They compound.

Chapter 20: The Legal Imperative — Contracts Under a Vacuous Unit

The legal mechanism:

- A valid contract requires determinate terms

- Determinacy requires the unit of denomination to have a valid intensional definition

- The conventional monetary unit has no valid intensional definition (Chapter 1)

- Therefore contracts denominated in conventional monetary units are indeterminate

- Indeterminate contracts are void from inception by quae ab initio non valent, ex post facto convalescere non possunt

- Knowledge of this void creates a binding legal obligation to seek remedy

- The passive unit specification provides the remedy

The Fungibility Failure: A Five-Step Legal Derivation

The Procedural Instrument

Acknowledge in writing: (1) that no valid formal definition of the monetary unit currently exists that is internally consistent, obeys natural law, and is wholly consistent with the terms of current monetary contracts; (2) that the operative notion of money constitutes a misrepresentation; (3) that this misrepresentation produces structural instability with consequences for every individual subject to it.

Log your demand and its response: moneytransparency.com/demand-registry

Chapter 21: Why Conventional Policy Cannot Succeed — The Structural Argument

Conventional monetary policy faces a structural impossibility at two independent levels:

Level 1 (Theorem 1, Corollaries 2 and 3): no parameter adjustment removes the instability while r > 0.

Level 2 (Chapter 13a): the signal on which those parameter adjustments are based — V = PQ/M — is formally indeterminate and cannot identify the state of the system being managed.

The instruments are structurally blind as well as structurally insufficient. Both grounds are independent and each is sufficient on its own.

Chapter 21a: That Which Is Void Cannot Be Validated by Its Consequences

The most persistent informal defence of money's misrepresentation is consequentialist: whatever its logical defects, the misrepresentation has been the engine of economic development. This chapter refutes that defence on six independent grounds.

1. Legal Closure

The progress defence is self-referential: it validates the misrepresentation by appealing to consequences measured in units produced by the misrepresentation. This is the vicious circularity of Chapter 3 operating as its own defence.

2. The Measurement Problem

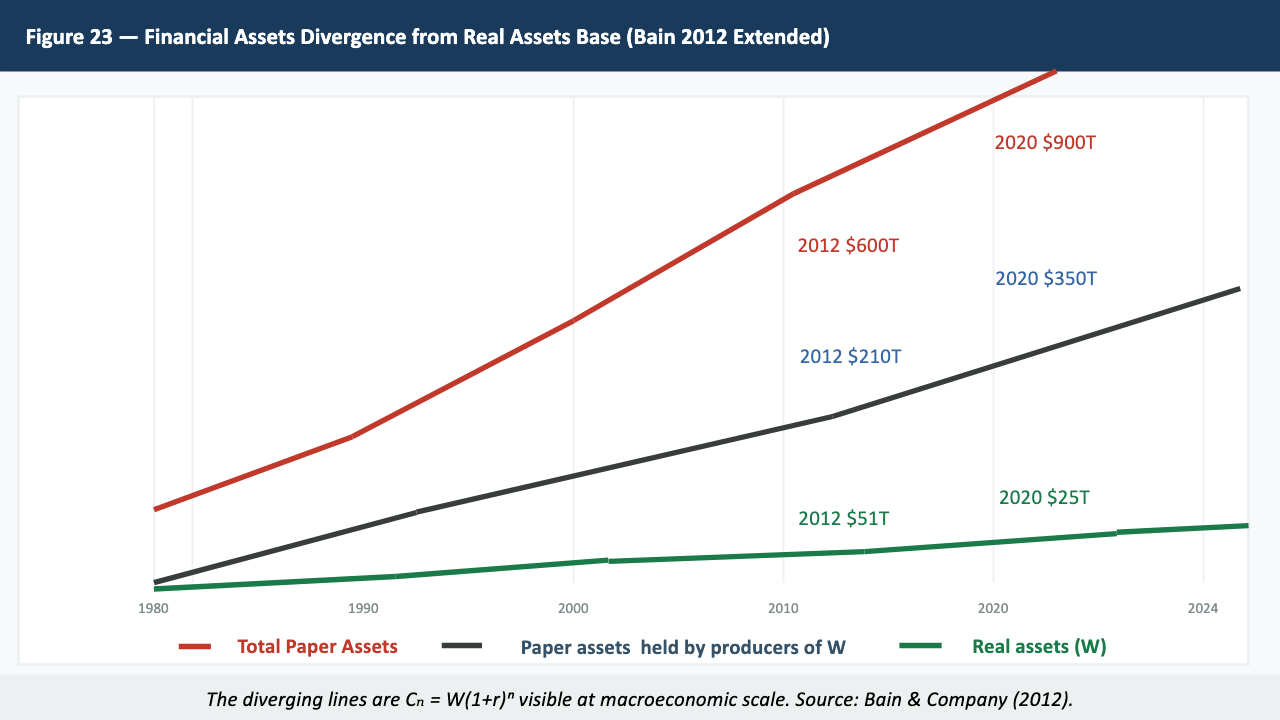

Global financial claims exceed global real assets by a factor of 3–10 (Bain & Company, 2012). The progress cited is an indeterminate mix of genuine productive development and phantom extraction, inseparable in void units.

5. The War Argument

The compounding mechanism applied to sovereign debt produces nominal obligations formally un-payable through any productive means. At some point the financial alternative to war appears more catastrophic to certain actors than war itself. War becomes structurally rational as a means of voiding unpayable obligations. The passive unit removes the rationality of war not by moral appeal but by eliminating the structural mechanism that produces it.

7. The Foreclosure of Optimum Response: Structural Cruelty as a Proved Consequence

Every person subject to the B>0 system rationally attempts to respond through the best available means: work harder, save more, invest wisely. But in a B>0 monetary system no optimum strategy exists for three independent structural reasons proved in this document: Cₙ diverges independently of every strategic variable; the instrument through which agents perceive the system is formally indeterminate; and every intervention transfers instability residue without reducing it.

Chapter 22: The UN Policy Framework — Normative Requirements

| Requirement | Content |

|---|---|

| 1. Formal Definition | All monetary units must satisfy all thirteen conditions of Chapter 18 |

| 2. Immediate Interim Passivity | All percentage-based transaction fees on cumulative transacted value must be eliminated |

| 3. Legal Validity | All new international contracts must be denominated in units satisfying Requirement 1 |

| 4. Transparency | All monetary system operators must publish complete formal specifications |

| 5. Natural Capital Accounting | Monetary accounting must record consumption of natural capital as a real cost component |

| 6. Technology Governance | No new financial technology increasing transaction velocity may be deployed without prior compliance with Requirements 1 and 2 |

| 7. International Monetary System | No monetary unit used in international trade may carry independent commodity value (B>0) |

| 8. Information Architecture | Public account balances; private transaction details |

Chapter 23: The Pivot — Why Correcting Money's Misrepresentation Is the Precondition for All Other Solutions

Every major challenge facing humanity — climate change, biodiversity loss, inequality, resource depletion, political instability, unsustainable debt, the risk of large-scale and nuclear war — has a monetary dimension and is partially driven by the structural imperatives generated by the misrepresented unit. None can be fully resolved while the misrepresentation remains in place.

The correct target for adoption is the definition of the monetary unit itself — the rules governing all transactions, not a subset. This is why the definitional correction is the precondition for all other solutions.

Network Clearing: A Withheld Efficiency

The principle of multilateral obligation netting — the automatic cancellation of offsetting obligations within cycles of three or more parties — is among the oldest known practices of economic organisation. The mathematics of cycle detection is computationally trivial. Yet it has never been extended to the productive agents whose obligations generate the transaction flows the interbank system clears on their behalf.

Every obligation netted rather than individually settled is a transaction on which no percentage fee is earned. The confinement of clearing to the interbank system is therefore not an accident of regulatory complexity — it is the structural consequence of the percentage-fee mechanism protecting its own extraction base.

The Human Dimension

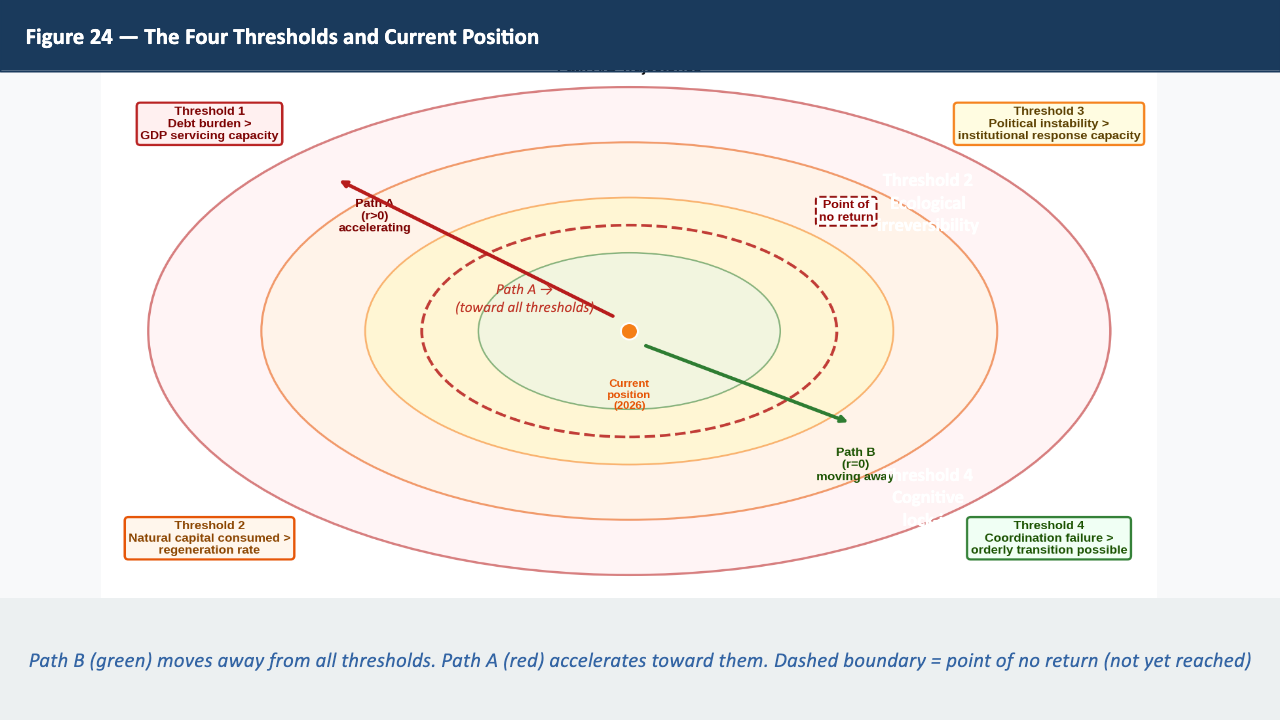

Chapter 24: The Point of No Return — Why We Have Not Yet Reached It

The point of no return is defined by four threshold conditions:

- Domain exhaustion — W falls below minimum required to sustain chains generating Cₙ

- Natural capital irreversibility — ecological tipping points permanently reduce V_max

- Institutional capture — institutions with authority to correct the unit become structurally dependent on extraction

- Cognitive lock-in — the population capable of recognising and acting on the FILP argument falls below critical mass

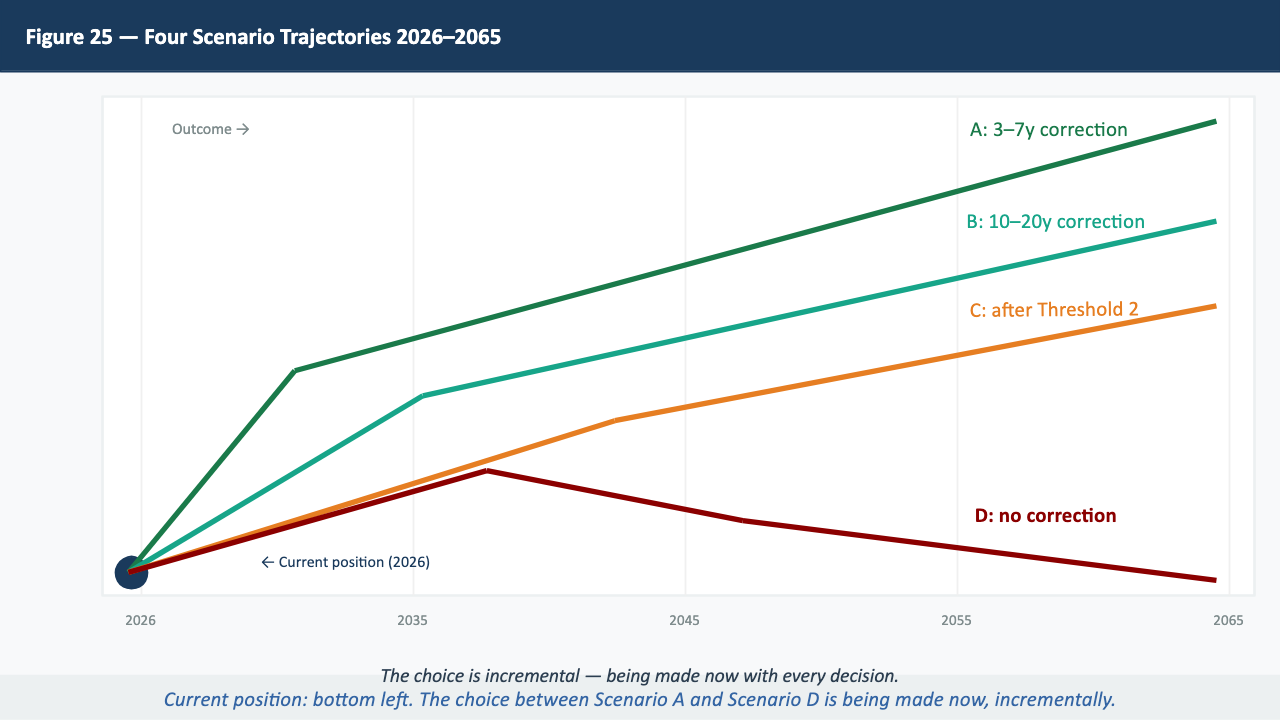

Chapter 25: The Timeline — Saved or Doomed

| Scenario | Correction Timeline | Outcome |

|---|---|---|

| A | Within 3–7 years | Survivable, approach to V_max possible |

| B | Within 10–20 years | Viable but permanently reduced domain |

| C | After Threshold 2 | Ecologically constrained but worth doing |

| D | No correction before Threshold 1 | Forced systemic collapse |

Current trajectory is toward Scenario B or C. Scenario A remains open but requires deliberate acceleration.

The Distribution Architecture: Word of Mouse

The MSTA argument reaches its audience through a heterogeneous network, not a hierarchical one. Distribution sequence: (1) the citizen letter to all immediate contacts; (2) the appropriate presentation to qualified contacts; (3) a demand letter to a monetary authority; (4) log at moneytransparency.com/demand-registry.

Chapter 26: Finite Costs, Infinite Value, and the Irreplaceable Human Node

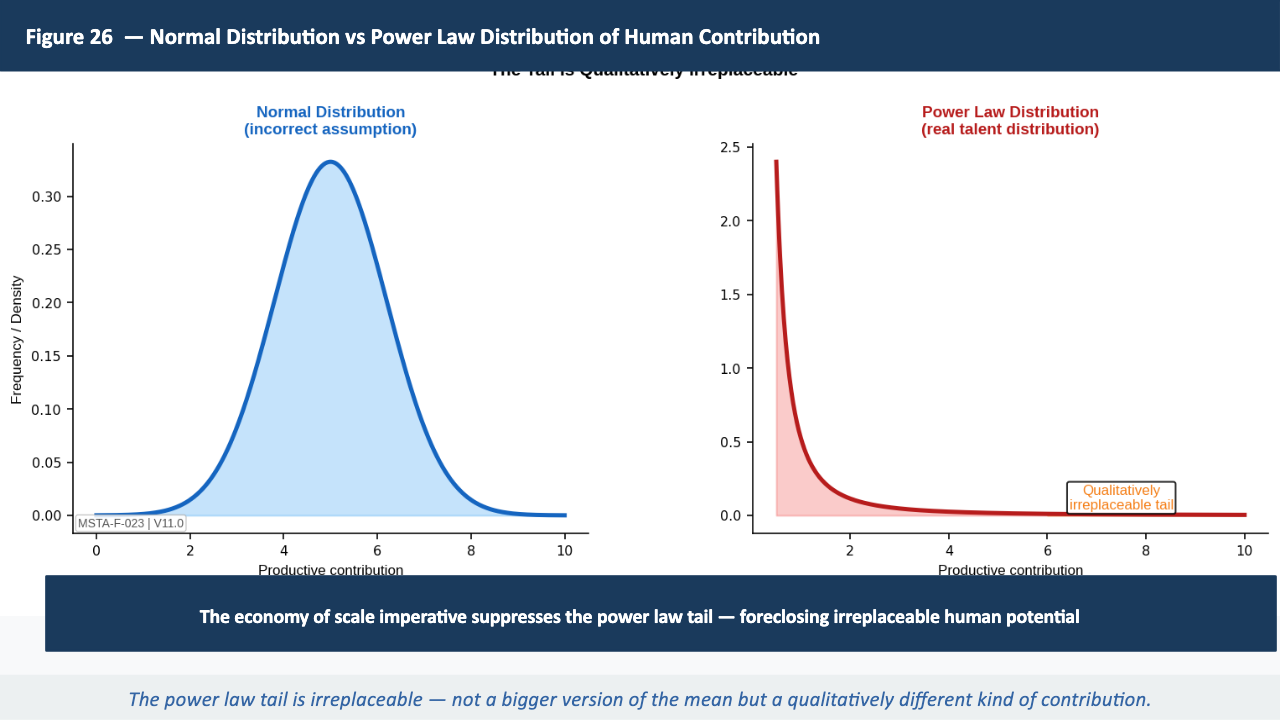

Value space partitions into X_physical — finite, measurable, bounded by V_max — and X_infinite — the creative, intellectual, and relational dimensions, formally unbounded. Human talent follows a power law distribution P(x) ∝ x^(−α).

In a power law with α = 1.5, the top 1% of contributors account for approximately 50% of total productive impact. These are not just larger contributors — they are qualitatively different kinds of contributors whose removal cannot be compensated by any multiplication of average contributors. The misrepresentation specifically suppresses this tail through the economy of scale imperative.

Chapter 26a: The Achievable Optimum — 18 Hours, Maximum Quality, and the Freedom to Flourish

Approximately 18 hours of productive effort per working-age person per week is sufficient to guarantee the highest achievable quality of essential needs for every human being, leaving the remaining two-thirds free for the unimpeded pursuit of each person's natural calling. This is a formal lower bound, not a utopian projection.

| Essential Category | Hours/week | Basis |

|---|---|---|

| Food (precision agriculture, processing, distribution) | 3 | FAO productivity data |

| Housing (modular construction, maintenance) | 2 | Construction technology benchmarks |

| Energy (renewable systems) | 2 | IEA renewable capacity data |

| Healthcare (preventive-first system) | 4 | WHO preventive care cost studies |

| Education (universal high-quality access) | 3 | UNESCO productivity benchmarks |

| Infrastructure and coordination | 4 | Engineering standards literature |

| TOTAL | ~18 | Conservative upper bound under r = 0 |

The world currently produces enough food to feed 10 billion people. Modern construction technology can house everyone. Renewable energy is sufficient. The failure is not a failure of production — it is a failure of distribution caused directly by the extraction mechanism consuming the productive surplus. Under r = 0 this contradiction disappears.

Conclusion: The Simplicity of the Remedy

Define the unit of money by what it is — a passive record of value given pending reciprocation — not by what it does as a commodity in a market it was supposed to measure. Ground the definition in independently determinable criteria so that every contract denominated in monetary units is decidable and legally valid.

These requirements cost nothing to implement. They penalise no agent. They require no transfer of wealth, no political consensus on values, and no agreement on what humanity should produce or prioritise. They require only logical consistency — the same standard applied to every other measurement instrument used in science, engineering, and law.

— MSTA Policy Document V16, Marc Gauvin, 2026

This document is submitted to the United Nations and to all institutions with monetary authority by Marc Gauvin, Money Systems Transparency Alliance (MSTA), 2026 — building on the Passive BIBO Currency Project initiated in 2009/2010 and on 44 years of formal development. The argument has not been refuted in any forum in which it has been encountered.

Glossary of Key Terms

| Term | Definition |

|---|---|

| BIBO Stability | Bounded-Input Bounded-Output stability. The monetary system with r > 0 is BIBO unstable: bounded real input W produces unbounded nominal output Cₙ = W(1+r)ⁿ. |

| B=0 Proof | A = A + B if and only if B = 0. A monetary unit is a valid measure of value A only if it carries no independent commodity value B. |

| Category Error | Treating a property of the range (nominal cost) as a property of the domain (real value), or treating a passive measure as an active commodity. |

| FILP | First Independent Logical Principles. Premises verifiable by anyone independently. Refutation requires identifying a specific logical error. |

| Intensional Definition | A definition specifying necessary and sufficient properties in independently determinable terms. |

| i_eff = r/τ̄ | The effective time-domain instability rate. As technology reduces τ̄, i_eff increases without bound for any r > 0. |

| Lebesgue Measure | Integration summing across value levels rather than along a path. A valid monetary measure satisfies Lebesgue conditions. |

| Passivity | Output ≤ input. A passive monetary unit charges fees grounded only in the measured cost of services rendered. |

| Quae Ab Initio Non Valent | Latin: that which is void from the beginning cannot be made valid by subsequent act. |

| Stein's Dirt | The conserved residue of feedback control: every conventional policy intervention moves instability without eliminating it. |

| Theorem 1 | Cₙ = W(1+r)ⁿ, proved by mathematical induction. BIBO stable only when r = 0. |

| V_max | The maximum total real value achievable from the biosphere's energy budget. The asymptotic ceiling of logistic value growth under r = 0. |

Mathematical Glossary for Non-Mathematical Readers

Every mathematical symbol and concept used in this document is explained here in plain language.

A = A + B if and only if B = 0

Elementary arithmetic: 5 = 5 + B is only true if B = 0. If B = 2, then 5 does not equal 7. This is the entire B=0 proof: the monetary unit can record the value A of goods transacted only if it adds nothing of its own (B = 0).

BIBO Stability (Bounded-Input Bounded-Output)

Imagine a thermostat: you give it a bounded input (a temperature setting) and it should produce a bounded output (actual room temperature). The monetary system with percentage fees is BIBO unstable: a constant bounded productive input W produces a nominal output Cₙ that grows without limit. Like a thermostat that sets your house on fire when you ask for 21 degrees.

i_eff = r/τ̄ (Effective Instability Rate)

Think of a leaking bucket: the rate at which it empties depends on both the size of the hole (r, the percentage fee) and how often you refill it (τ̄, transaction time). As electronic payments reduce τ̄ toward zero, the instability rate i_eff increases without bound for any hole size r > 0 however small.

r_attenuation (Attenuation Cost)

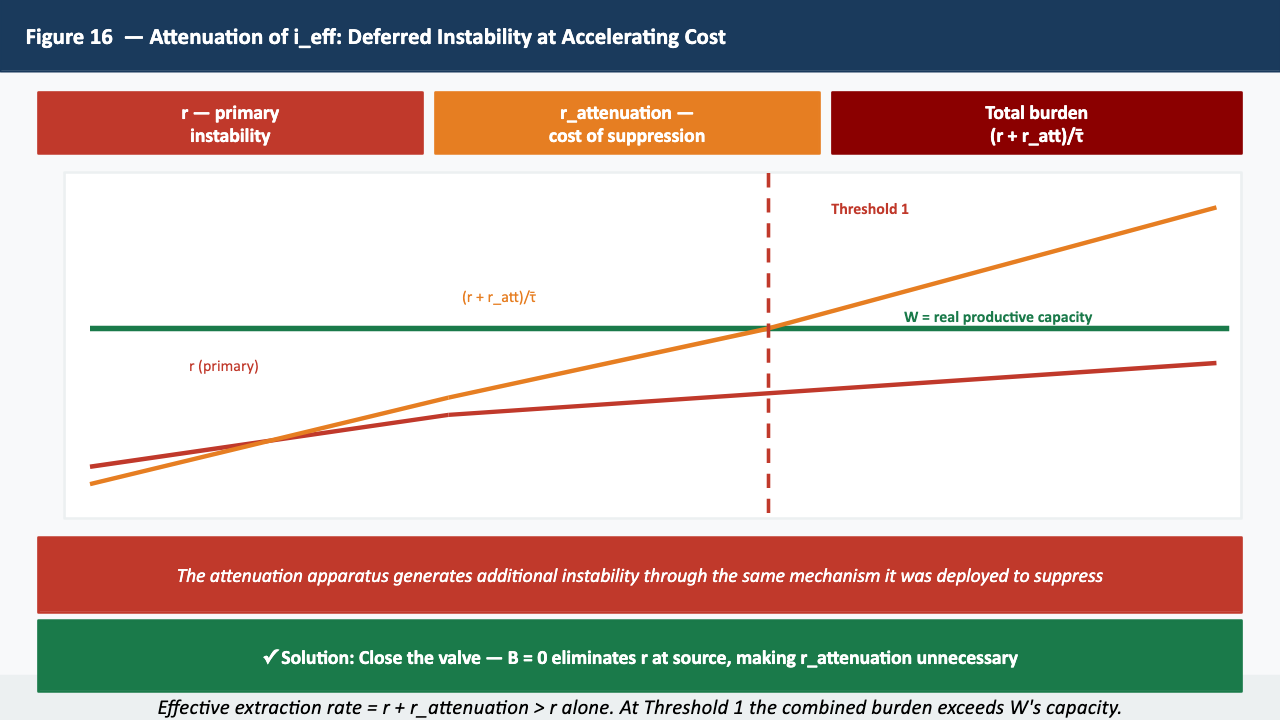

The aggregate percentage cost of policy interventions deployed to suppress the visible expression of the primary instability. QE, bailouts, sovereign debt service, inflation, taxation — all are percentage-based extractions on productive activity. The effective extraction rate is therefore not i_eff = r/τ̄ alone but (r + r_attenuation)/τ̄.

The Lebesgue Integral V(A) = ∫_A u(x) dμ(x)

Two ways to add up a pile of coins: Riemann adds them left to right along the path. Lebesgue groups them by value first (all the 1p coins, all the 2p coins) then adds. Both give the same total only if no coin changes value during counting. A percentage fee is like a coin that changes value depending on which coins are already in the pile.

M ∩ C = ∅

Two circles on a Venn diagram that do not overlap. M is the set of properties a valid measure must have. C is the set of properties a commodity has. These two circles share no properties. Anything that is both a measure and a commodity belongs to both circles simultaneously — a logical contradiction.

Mathematical Induction

A method of proof that works like dominoes. Show that the statement is true for n = 1 (knock over the first domino). Show that if it is true for n = k, it must also be true for n = k+1 (each domino knocks over the next). If both steps succeed, the statement is true for all n. Theorem 1 is proved this way.

The Radon-Nikodym Derivative dν/dμ

Imagine two rulers measuring the same wall. A valid relationship between them requires that wherever Ruler 1 measures zero length, Ruler 2 also measures zero. The percentage fee violates this: the nominal ruler (Ruler 2) measures growing value even when the real ruler (Ruler 1) measures zero new production.

Power Law Distribution P(x) ∝ x^(−α)

Compare two distributions. Normal (bell curve): most people are near the average, extremes are rare. Power law: most are small, but the occasional extreme is orders of magnitude larger than the average. The composer who transforms music for centuries is not a bigger version of an average composer — they are a qualitatively different kind of contributor.

V = PQ/M (Velocity of Money)

A ratio of two numbers: total nominal transactions divided by total money supply. Like measuring traffic flow by dividing total distance driven by number of cars, without knowing whether one car drove almost all of it or every car drove equally. The same ratio V = 1.0 can represent a healthy economy or a dysfunctional one with extreme concentration. The formula cannot tell the difference. It is indeterminate.

η(n,r) — System Efficiency

The ratio of real value delivered to nominal claim after n periods at rate r:

At empirically calibrated values (r = 0.03; n = 50): η ≈ 0.23. Approximately 23% of current productive capacity reaches real value; the remaining 77% services the extraction imperative or dissipates as Stein's dirt.

References

Passive BIBO Currency and MSTA Publications

Gauvin, M. (2013). 'Bitcoin in Light of Passive BIBO Currency.' bibocurrency.com.

Gauvin, M. (2012). The Money PSYOP. Gauvin McNeill, Alicante.

Gauvin, M. (2014). 'Money: Commodity or Measure — Not Both.' bibocurrency.com.

Gauvin, M. & Domínguez, S. (2020). A Systems Engineering Approach to Formal Monetary and Financial Stability. MRC UNWE, Sofia.

Gauvin, M. & Domínguez, S. (2011). 'ASTA3 Requirements for Passive BIBO Stable Currency System.' bibocurrency.com.

Gauvin, M. & Domínguez, S. (2012). 'Formal Passive BIBO Currency Specification.' bibocurrency.com.

Control Systems and Stability Theory

Desoer, C.A. & Vidyasagar, M. (1975). Feedback Systems: Input-Output Properties. Academic Press.

Stein, G. (2003). 'Respect the Unstable.' IEEE Control Systems Magazine, August 2003: 12–25.

Willems, J.C. (1972). 'Dissipative Dynamical Systems.' Archive for Rational Mechanics and Analysis 45: 321–393.

Mathematical Foundations

Lebesgue, H. (1902). 'Intégrale, longueur, aire.' Annali di Matematica Pura ed Applicata 7(1): 231–359.

Radon, J. (1913). 'Theorie und Anwendungen der absolut additiven Mengenfunktionen.'

Rudin, W. (1987). Real and Complex Analysis (3rd ed.). McGraw-Hill.

Financial Claims and Real Assets

Bain & Company. (2012). A World Awash in Money: Capital Trends Through 2020.

Bank for International Settlements. (2024). Annual Economic Report. BIS, Basel.

Legal Standards

European Union. Directive 2013/34/EU (Accounting Directive), Article 4.

Spain. Código de Comercio, Article 34; Código Civil, Arts. 1272, 1753.

Bell v Lever Brothers [1932] AC 161; UCC § 1-201(24).

Appendix A: A Brief History of Money's Misrepresentation

This appendix traces the historical origins of the monetary misrepresentation. Its purpose is not to establish the argument — the argument stands on FILP independently of any historical account — but to show that the error is ancient, persistent, and has survived every monetary reform attempted to date precisely because those reforms addressed the governance of the misrepresentation rather than the misrepresentation itself.

1. Pre-Monetary Value Recording: The Passive Origin

Clay tokens found throughout the ancient Near East from approximately 8000 BCE onward served as records of goods held or owed. Each token represented a specific quantity of a specific good. The token did not have value in itself: it recorded value, pending reciprocation. It was, in the precise formal sense of Chapter 18, passive — B=0 by construction.

2. Fungibility and the First Step Toward Misrepresentation

As the range of trade expanded, the most desired and durable fungible commodities — gold and silver — became the universal standard. Aristotle identified money's purpose as to "measure all things." This attribution corresponds to the first formal manifestation of money's core logical misrepresentation: the conflation of money as a commodity in trade with money as a standard measure.

3. Mesopotamia: The First Compounding and the First Law Against It

The earliest recorded instance of compound interest appears in Early Dynastic Mesopotamia, approximately 2400 BCE. The Code of Hammurabi (approximately 1760 BCE) represents the first known legal attempt to regulate this instability. Debt cancellations ("jubilees") were periodically declared precisely because compounding debt had accumulated beyond the productive capacity of the agricultural economy to service it — Stein's dirt transfer, not elimination.

4. Classical Antiquity: Aristotle's Insight

Aristotle condemned usury as unnatural: money as a measure has no natural reproductive capacity, and charging interest treats it as if it did. This is a direct anticipation of the B=0 requirement. He lacked the formal algebraic apparatus to prove it, but the intuition is exact.

8–9. The Gold Standard and Bretton Woods

Gold has independent commodity value B>0. The gold standard did not correct the logical error — it embedded the error in a physical substrate. On 15 August 1971, Nixon suspended dollar-gold convertibility, completing the transition to a fully fiat global monetary system with no physical anchor whatsoever.

10. The Digital Age: Acceleration Without Correction

CBDCs without a passive unit specification (B=0) will accelerate instability by reducing transaction time toward zero while leaving r>0. A CBDC without a passive unit definition is not a monetary reform. It is an acceleration of the existing misrepresentation with greater surveillance capacity attached.

The Pattern Across Ten Millennia

The passive origin → the misrepresentation enters → instability follows → reforms address governance, not definition → the misrepresentation persists. Because the logical error is never corrected at the definitional level, it survives every reform and reconstitutes itself in the next institutional form.

Appendix B: Falsifiability Register

This appendix maps every substantive assertion to its mathematical or logical basis, its type, and the precise condition that would falsify it. Every claim is either logically necessary (denial leads to contradiction), mathematically proved (falsifiable only by error in the proof), or empirically grounded (falsifiable by contrary observation).

| Assertion | Claim | Type | Falsifiability Condition | Status |

|---|---|---|---|---|

| A1 | No valid intensional definition of money exists | Empirical | Provide necessary and sufficient conditions in non-circular terms | Unfalsified |

| A2 | M ∩ C = ∅: measure and commodity properties are disjoint | Logically necessary | Identify a property coherently belonging to both without contradiction | Unfalsifiable |

| A3 | Theorem 1: Cₙ = W(1+r)ⁿ, BIBO unstable for r>0 | Proved by induction | Demonstrate error in inductive step | Unfalsified |

| A4 | Radon-Nikodym derivative does not exist for percentage fee | Mathematically proved | Identify real domain activity corresponding to Fₙ at empty activity set | Unfalsified |

| A5 | B=0 is necessary and sufficient for valid measure | Logically necessary | Demonstrate A = A + B for B>0 | Unfalsifiable: requires 5 = 7 |

| A6 | V=PQ/M is formally indeterminate | Proved by construction | Demonstrate V uniquely identifies economic activity distribution | Falsified in positive direction |

Category Summary

Category I — Logically Necessary: A2, A5, A11, A22, A23, A24. Cannot be falsified as denial requires arithmetic or logical impossibility.

Category II — Mathematically Proved: A3, A4, A6, A7, A10, A14, A15, A16, A17a. Stand until a specific error in the proof is identified. None has been.

Category III — Empirically Grounded and Confirmed: A1, A8, A9, A12, A17b, A21.

Appendix C: Methodological Objections and Responses

O-1. The Transition Objection

"Even granting the proof, moving from B>0 to B=0 would require cancelling the existing global debt and contract structure — a practical impossibility."

This objection confuses structural correction with operational disruption. The passive unit remedy requires no cancellation of existing contracts, no revaluation of existing wealth, and no intervention in productive activity. It requires only that new transactions be governed by passive rules.

O-5. The Scope-of-Domains Objection

"Chapter 13 identifies six domains where the category error recurs. Are there domains where the monetary instability does NOT propagate?"

For all domains not fully isolated from the monetary system, the systems principle applies: any instability either is cancelled at a cost, or propagates. If the cancellation cost constitutes any ongoing overhead with percentage-based pricing, the cancellation mechanism is itself a source of instability.

O-8. The Axiom of Money's Function Objection

"What if money's function is not measurement but social coordination, in which case no metrological requirement applies?"

If money's function is purely social coordination with no formal criterion, then: (a) no contract has determinate truth conditions; (b) no monetary policy instrument has a determinate target; (c) the instability proof remains intact. The objection arrives at the same conclusions by a different route.

O-12. The Modern Monetary Theory Objection

MMT does not alter the unit definition. It takes the existing B>0 unit as its operating instrument. Since B>0 is sufficient alone to produce Cₙ = W(1+r)ⁿ instability regardless of who issues the units or in what quantity, MMT is necessarily unstable by Theorem 1. Sovereign issuance does not cure B>0 because B>0 is a property of the unit itself, not of the institution that issues it.

O-13. The Cardinal Measurability of Value Objection

"The ordinalist revolution demonstrated that utility need only be ordinal. The effort-induced measure commits the interpersonal comparison error."

The ordinalist critique is directed at the measurement of internal subjective utility states. The effort-induced measure μₑ does not measure internal states. It measures the physical allocation of effort across outcomes — independently observable without reference to anyone's internal experience. The interpersonal comparison objection misidentifies what is being measured.

Furthermore: if the objection were correct and value were genuinely cardinally unmeasurable, the consequences for the current monetary system would be more severe, not less. An instrument that claims to measure something unmeasurable is not merely poorly calibrated — it is making a claim that is in principle unverifiable. The ordinalist position, if accepted, condemns the current monetary unit more thoroughly than Chapter 1a does.

MSTA Policy Document V16 · Marc Gauvin · 2026

Money Systems Transparency Alliance

moneytransparency.com ·

bibocurrency.com

Get the Materials ·

Register Your Demand